Why NVIDIA’s Post-Earnings Flatline Signals a Major Buying Opportunity

How NVIDIA builds its own cloud, strips market share from AMD and Intel, and launches its robotics monetization engine

NVIDIA stock barely reacted to its Q1 FY27 earnings report. The shares are flat-lining, and that is the market’s biggest strategic blunder right now. Investors are obsessively trying to predict a “CapEx cliff” and a plateau in spending by Microsoft or Google, fearing an imminent drop in demand for GPUs. But Jensen Huang is three steps ahead

These financial results belong to the sovereign ruler of computing infrastructure. NVIDIA is actively engineering its own demand, laying the foundation for a $4 trillion market, and systematically dismantling the business models of legacy competitors.

Capital Dominance: How to Engineer Your Own Buyers

NVIDIA is using its balance sheet as a first-strike financial weapon. In a single quarter, the company deployed $40 billion in direct equity investments into partner companies and specialized infrastructure funds. This capital went straight to the key players in the Neo-Clouds: Nebius, CoreWeave, and IREN

This is a ruthless strategic calculation with a triple-threat effect:

Guaranteed supply absorption. The recipients of these investments are contractually obligated to build their data factories exclusively on the CUDA architecture. Huang has created a loyal pool of buyers, completely insulated from any attempts by Big Tech to transition to in-house silicon.

Monopolizing energy grids. The ultimate bottleneck in the AI industry is access to electricity. Independent cloud providers use their long-term NVIDIA chip delivery contracts as high-grade collateral. Using this leverage, they secure billions in debt financing and lock down grid access commitments from global utility companies before anyone else can.

A distribution channel for frontier developers. Pure-play AI clouds operate without the heavy legacy infrastructure of traditional web services. They deploy computing capacity in record time, making them the preferred partners for elite AI labs like Anthropic and Perplexity.

Breaking the Big Tech Monopoly

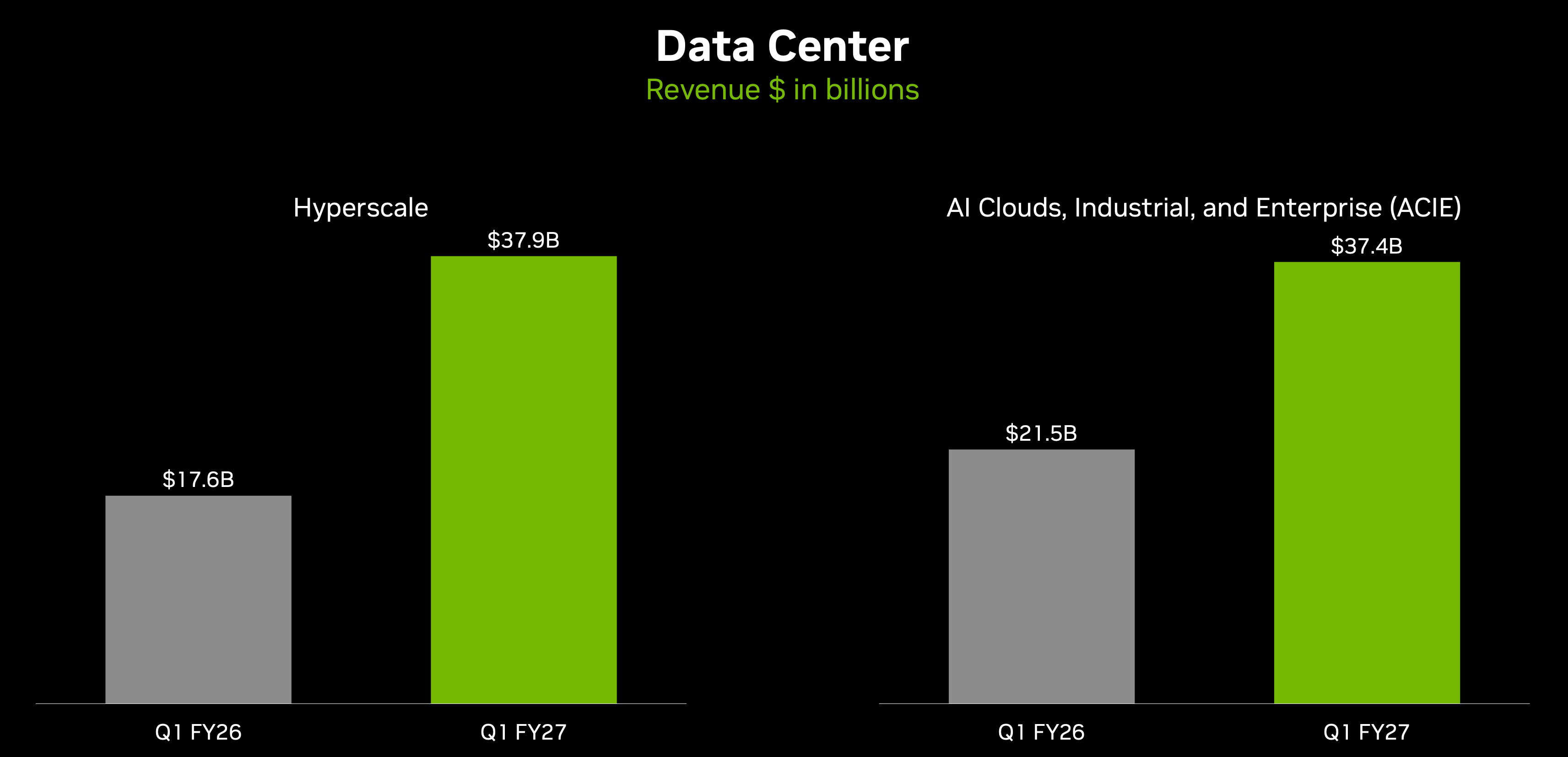

For a long time, NVIDIA’s primary vulnerability was customer concentration—relying on just four or five massive tech companies for nearly all of its revenue. The Q1 report officially marks the end of this risk. Now, datacenter revenues are split into two comparable segments: traditional Hyperscalers and ACIE (Alternative Clouds, Industrial, & Enterprise).

The revenue splits have achieved near-parity:

The growth of the ACIE segment ($37.38 billion, +31% QoQ) is impressive, but it must be viewed as a defensive buffer against the inevitable loss of traditional Hyperscaler volume ($37.87 billion, +12% QoQ). Big Tech is actively building a parallel supply chain:

The TPU and ASIC Insurgency: Google is aggressively scaling its TPU v5p and v6e architectures. Amazon is deploying Trainium2 and Inferentia, while Microsoft scales its Maia silicon. These chips do not need to outperform NVIDIA on raw specs; they only need to offer superior price-to-performance for specific internal workloads. Every workload migrated to in-house silicon permanently erodes NVIDIA’s addressable market.

The Blackstone-Google Alliance: Hyperscalers are bypassing NVIDIA’s land-and-energy grab through massive direct partnerships with infrastructure capital. Google’s collaborative data center play with Blackstone and other energy-infrastructure giants bypasses the Neo-Cloud proxy network entirely. By building massive, customized data center campuses optimized specifically for in-house TPUs, hyperscalers are securing gigawatt grid allocations

The Software Decoupling (XLA and PyTorch): The real moat has always been CUDA. However, the industry is aligning around open-source compilers like Google’s XLA (Accelerated Linear Algebra) and PyTorch 2.0. These frameworks allow developers to compile models directly to custom ASICs with minimal code modification, steadily diluting the developer-lock that historically kept customers tied to NVIDIA hardware.

Evicting x86: The Vera CPU Conquest

NVIDIA is claiming the traditional server CPU market with its new Vera processor. Management officially confirmed visibility to roughly $20 billion in standalone sales for Vera this year alone.

The scale of this move is massive: the annualized sales of this single product immediately match AMD’s entire datacenter segment. With a total addressable market for server CPUs exceeding $200 billion, NVIDIA has immense room to expand. This is an architectural necessity for the era of Agentic AI.

But it comes with a price. NVIDIA’s Vera is built on the ARM architecture, but hyperscalers have been optimizing their own custom ARM CPUs for years. Google’s Axion, AWS’s Graviton4, and Microsoft’s Cobalt 100 are already deployed at scale. These custom CPUs handle general-purpose cloud workloads and node orchestration at a fraction of the cost of merchant silicon. Introducing a premium, third-party CPU like Vera faces direct internal resistance within hyperscaler datacenters

Intel and AMD still control the vast majority of legacy enterprise server infrastructure. Enterprise database migration from x86 to ARM is notoriously slow, costly, and complex. While Vera may succeed in pure-play AI environments, capturing general-purpose enterprise CPU workloads requires displacing entrenched legacy architectures with decade-long software support cycles.

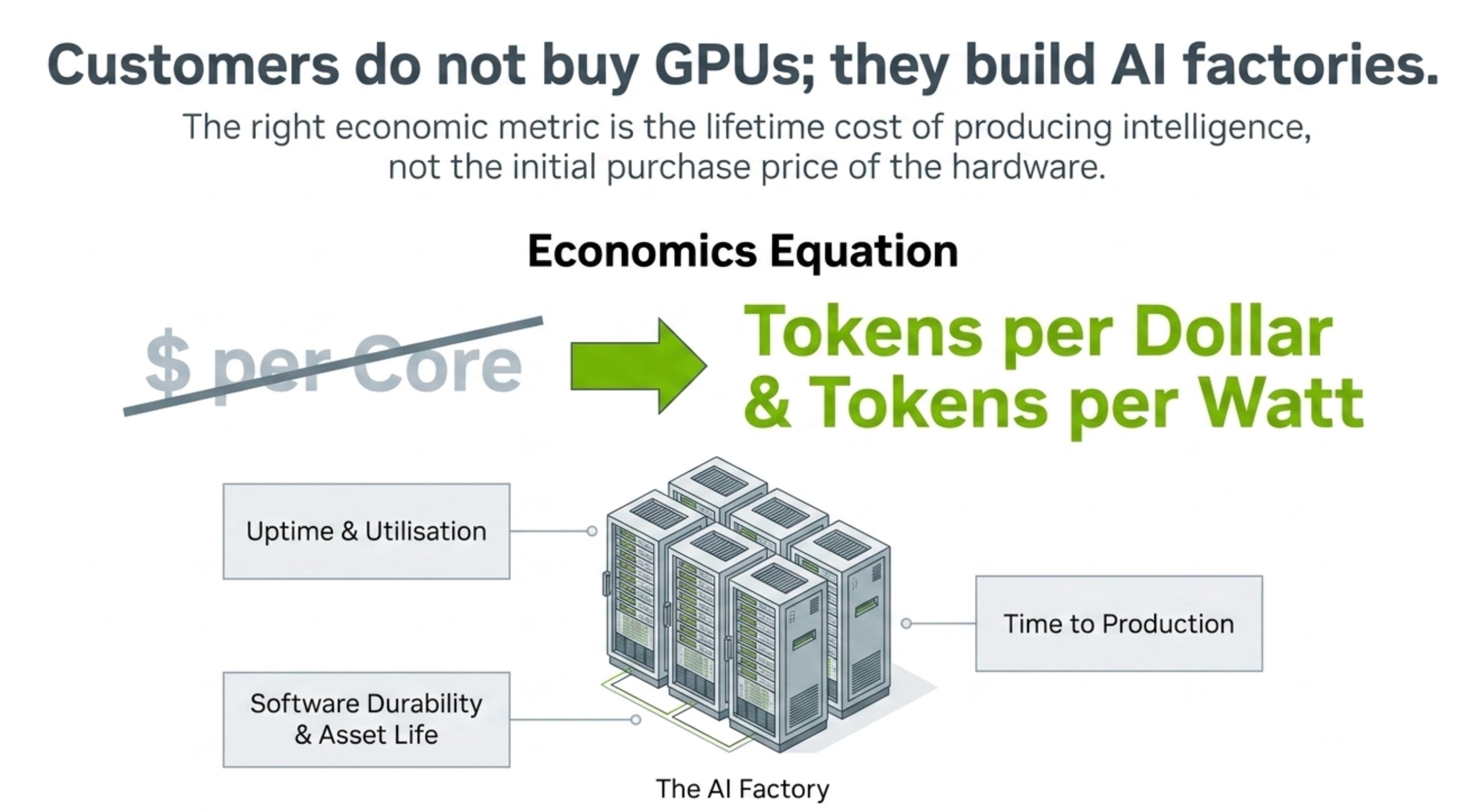

Physical AI: The Brain for the Real World

While venture capitalists argue over the capabilities of text-based language models, NVIDIA is taking over the physical world. Physical AI and robotics have become the third core pillar of the company’s long-term strategy to embed the CUDA architecture into cars, factories, medical instruments, and drones.

When I talk about physical AI, and I talk about how the rest of the $100 trillion industry that has not been impacted by IT in the last 30 years, it’s about to be impacted by AI. That is the segment that I’m talking about. The second cluster is growing incredibly fast. Our share of that, of course, is very large. We’re fairly unique in our ability to be able to serve this industry. Our platform is built like it’s vertically integrated so that everything works. Jensen Huang

This segment transitioned out of research experiments long ago and is already generating over $9 billion in annualized revenue. The growth is fueled by long-term software integration contracts and massive infrastructure partnerships, including the deployment of Uber’s robotaxis across 30 cities by 2028. By controlling the simulation software (Omniverse) and the physical processors that run the machines, NVIDIA guarantees its leadership in the next wave of the technology cycle when the hype around generative software cools down.

The Loop

NVIDIA is generating an unprecedented $48.6 billion in free cash flow per quarter. These resources are being deployed to lock out any moves by potential competitors.

The company has locked down $145 billion in outstanding commitments, prepayments, and inventory. NVIDIA is buying up advanced packaging slots at TSMC and high-bandwidth memory (HBM3e/HBM4) supply capacity years in advance. Other players are physically blocked from scaling up alternative hardware production.

At the same time, proxy clouds like Nebius, CoreWeave, and IREN are leveraging their guaranteed chip allocations as collateral to reserve grid capacity from utility companies globally, totaling approximately 15 Gigawatts not counting 10 GW from Oracle

This is a flawless, self-sustaining loop: NVIDIA injects capital into partners ➔ partners leverage their hardware supply contracts to lock down scarce global energy and buy more chips ➔ the revenue loops back into the ACIE segment ➔ NVIDIA grows its free cash flow and pre-emptively buys out more factory capacity.

Investors are making a mistake by evaluating NVIDIA through legacy semiconductor metrics. Jensen Huang controls a $145 billion supply chain runway, directly distributes 25 gigawatts of scarce global electricity through proxy cloud networks, dictates new server architecture standards via the Vera CPU, and is capturing physical robotics.

Jensen Huang has built an aggressive, capital-recycled ecosystem to defend his market share. However, this strategy is balanced against a highly motivated hyperscaler cartel that is weaponizing custom silicon, forming direct energy alliances with global capital providers, and building open-source software bridges to bypass the CUDA moat. NVIDIA’s sovereign cloud cartel has secured a commanding lead, but the capital-intensive war for the future of global computing has only just begun.

Personally, I am gonna hold NVDA and will not sell the industry leader, even if it means missing out on gains from other stocks. In my view, these shares form the foundation of a core portfolio, and the earnings report once again confirms that the company is not standing still, but is actively shaping new markets around itself. Chasing maximum possible returns never ends well, so I hold common stock and purchase LEAPS on pullbacks (170–180) or breakouts (200+).

This publication is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Readers are solely responsible for their own investment decisions. The author holds positions in NVidia, IREN and Nebius.