NVIDIA Drafts IREN for the Power Grab: Will the Stock Price Follow?

NVIDIA is assembling its Shadow Cloud against competitors, which could help IREN secure new deals.

The AI revolution has entered a phase where capital is no longer the primary constraint, physical infrastructure and strategic energy access are. NVIDIA is moving past being a mere component supplier to Alphabet and Amazon. By backing players like IREN, CoreWeave, and Nebius, Jensen Huang is effectively building a “Shadow Cloud” designed to strip power from Google Cloud and AWS.

This is a defensive and offensive masterstroke. While the “Big Three” attempt to bypass NVIDIA with proprietary chips (TPUs, Trainium), NVIDIA is counter-attacking by creating a rival ecosystem.

By funneling $2.1B into IREN, NVIDIA ensures that the most advanced Blackwell hardware stays within its own “DSX” architecture, building a private army of infrastructure providers that cannot be held hostage by the software preferences of the legacy hyperscalers.

The “Holy Trinity” and the 600,000 GPU Ambition

NVIDIA has established a global axis of power to commoditize the cloud:

CoreWeave: The North American specialist.

Nebius: The European AI-native cloud.

IREN: The massive-scale utility powerhouse.

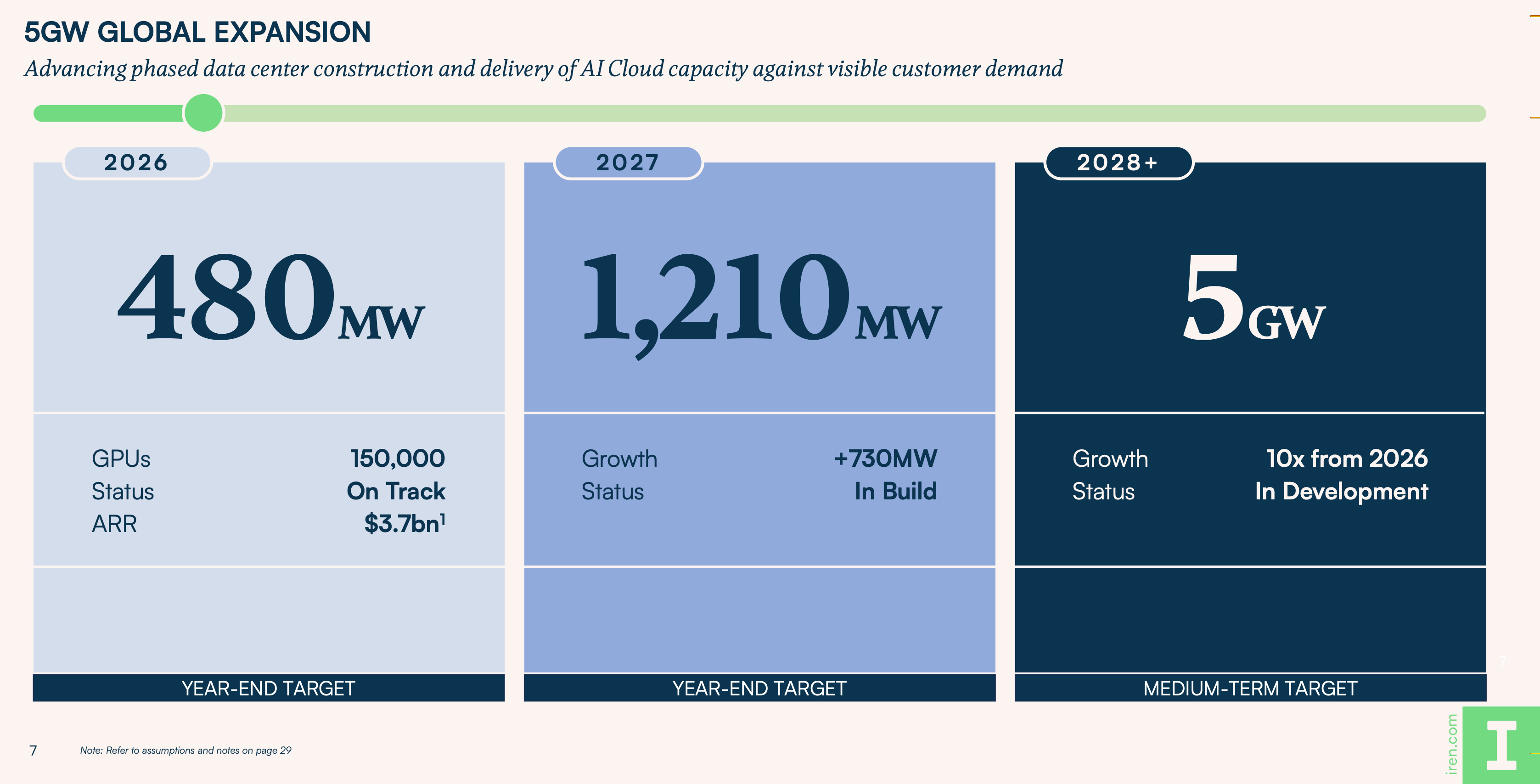

The defining factor for IREN is its target scale: 600,000 GPUs. To put this in perspective, this capacity would place IREN among the largest AI compute clusters globally, rivaling the internal infrastructure of the hyperscalers themselves. For NVIDIA, having 600,000 of its high-end GPUs controlled by a partner with its own 5GW power pipeline is the ultimate insurance policy against Hyperscalers and other chipmakers.

For IREN, the move into Spain via the Ingenostrum acquisition is a geopolitical pivot. By seizing 490MW in Europe and 5GW of total grid-connected capacity, IREN sidesteps US power constraints. This “golden ticket” access to Blackwell chips allows IREN to offer AI training to European enterprises faster than American giants can clear local power grid delays.

Helping hand

The most critical takeaway from the recent IREN earnings call is the depth of their integration into the NVIDIA ecosystem. IREN has moved beyond the phase of complex preliminary negotiations; they are now in a position to selectively “pick and choose” which Tier-1 clients to serve.

As Co-CEO Dan Roberts noted, negotiations are significantly streamlined when a provider has a proven deployment record and a transparent timeline. This marks a massive strengthening of IREN’s engineering capabilities, a sector where they previously lagged behind incumbents like CoreWeave and NEBIUS.

Dan Roberts: “This, again, is part of the close working relationship we’ve got with NVIDIA. You know, we’ve spent a lot of the last fortnight in their San Jose office working through how we service all types of customers, all the way from the trillion-dollar hyperscalers through to the emerging AI scale-ups, where a lot of this innovation and development is taking place. It’s funny, speaking to someone the other day, you don’t need a sales team in this market, particularly when you’ve got NVIDIA. "

Closing The Gap

IREN has historically lagged behind AI-native players like CoreWeave and NEBIUS in engineering depth. However, the recent earnings call signaled a massive strengthening of these capabilities:

The Engineering Gap: The acquisition of Mirantis and the deployment of the first GPU clusters indicate that IREN is closing the gap. As Co-CEO Dan Roberts noted, negotiations are significantly easier when you have a proven deployment record and a clear timeline.

The Competition: While IREN’s recent $3.4B deal is a strong signal, it must be viewed against HUT’s recent $10B deal and Nebius’ deals with META. IREN is operating in a crowded environment where “land and power” are no longer enough; they must prove they can win against incumbents securing even larger contracts.

Revenue Reality: The $33.6M in current AI revenue is a small fraction of the projected $3.7B ARR. The transition depends entirely on a flawless roll-out of the Blackwell clusters. Despite the headline $247.8M net loss in Q3 FY26, primarily a result of non-cash impairments on legacy mining hardware, IREN maintained an Adjusted EBITDA margin of 41%.

This proves that the core infrastructure business remains profitable even amidst a capital-intensive structural transition. However, the primary interest for institutional investors lies in the comparison with pure-play AI-Cloud providers. Currently, CoreWeave operates at 56% EBITDA margin. This 15% (1,500 bps) gap represents the immediate upside:

Normalizing the Mix: The 41% margin is “blended,” weighed down by legacy mining. As AI revenue becomes the dominant share, the margin is structurally positioned to converge toward the 56% benchmark.

Vertical Leverage: By deploying hardware on proprietary infrastructure rather than leased space, and utilizing the Mirantis software layer, IREN can optimize unit-level OpEx. Closing this 15% gap on a multi-billion dollar revenue base is a massive lever for earnings growth.

Capex is the big concern

The lack of explicit CAPEX guidance for the full 600k GPU build-out is a primary concern for institutional investors.

Capital Gap: Reaching the $3.7B ARR goal will likely require $3.5B–$4.2B in additional liquidity.

ATM Program: The $6B ATM program creates a persistent “overhang” on the share price. We model a fully diluted share count expansion to 450M-500M shares, which significantly dilutes the “per-share” value of the future ARR.

Re-evaluating the “NVIDIA Signal”

NVIDIA’s option to invest at $70 per share should be viewed as a Strategic Validation Signal rather than a guaranteed floor:

Warrants vs. Commitments: This is a “Godfather offer” designed to ensure IREN’s loyalty to the NVIDIA stack. It confirms that NVIDIA values the potential of IREN’s 5GW capacity.

Risk/Reward: If IREN fails to deliver on its engineering milestones or thermal management of 600k GPUs, even NVIDIA’s endorsement won’t protect the stock from a significant re-rating.

Forward Valuation (FY 2027 Estimates)

We apply a Forward P/S multiplier to the $3.7B ARR, adjusted for the projected 450M fully diluted share count.

However, the path to the $70-80 range depends on IREN proving it can move beyond “land and power” to become a reliable operator without drowning its shareholders in new stock issuances. Investors must weigh the $70 strategic anchor against the massive execution risks and aggressive moves by competitors like HUT and Nebius.

We are no longer in a chip war; we are in a global energy and infrastructure land grab. IREN’s 5GW pipeline and 600,000 GPU ambition make it a valuable asset to NVIDIA’s “Shadow Cloud” strategy.

This publication is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Readers are solely responsible for their own investment decisions. The author holds positions in IREN, Google, Amazon, Nebius and NVIDIA at the moment of the publication.

Good work. On the surface they all look like friends but NVIDIA really is making sure their chips gets used. At the same time though I think Google isn’t as concerned with chip market yet but rather wants to kill OpenAI with Anthropic on the same Brute-Force compute strategy. Idk just a theory…