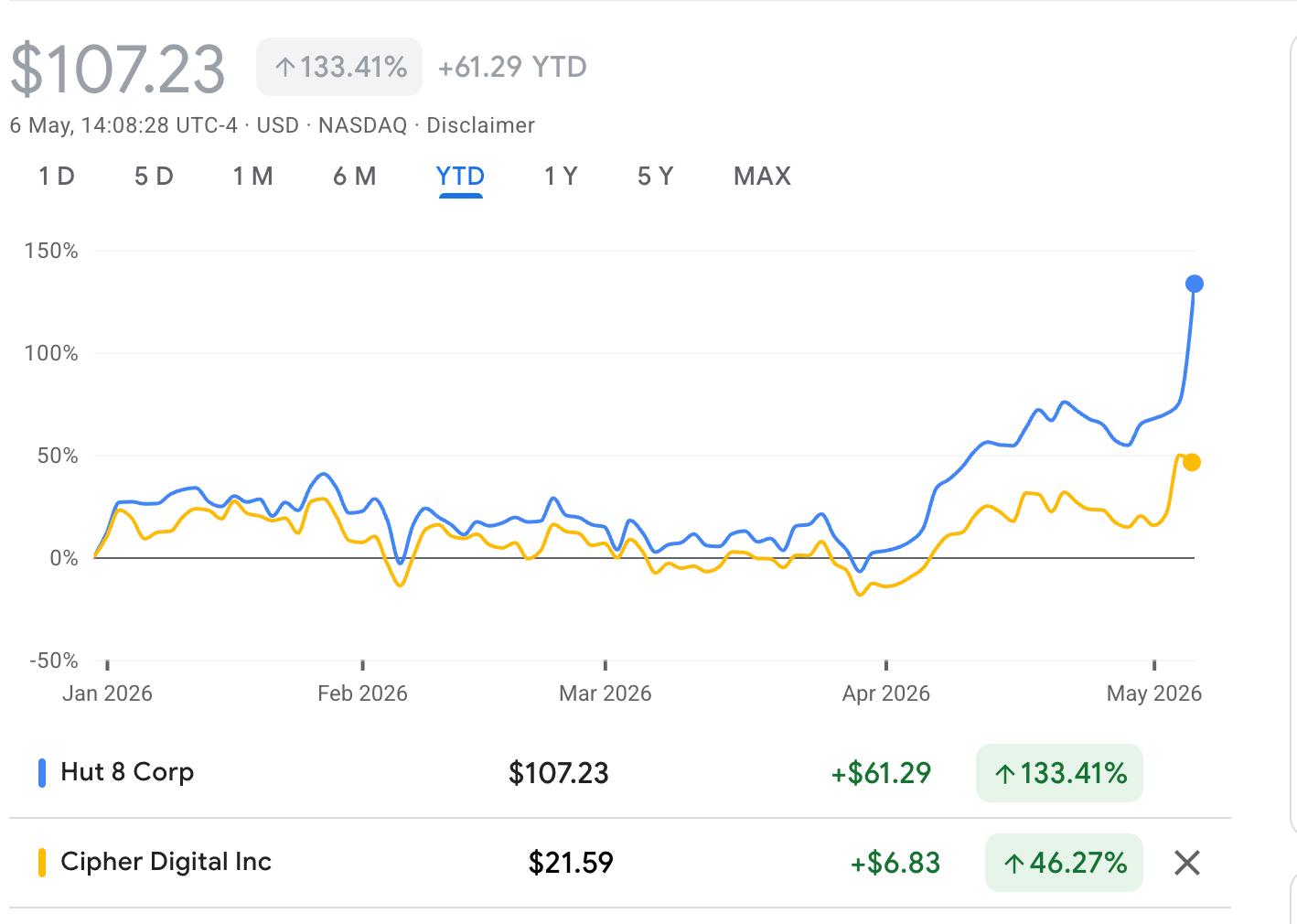

Why Hut 8 is Selling Better Than Cipher Mining

Why Cipher is pivoting its business model and do they have the cash to pull it off?

The U.S. digital infrastructure sector is colliding with a physical reality check. Goldman Sachs projects that data center power consumption will surge to 8.5% of total domestic demand by 2027, a structural shift that threatens to fracture the national energy map.

This rapid doubling of capacity will not be felt evenly; instead, it is creating a stark geographical disparity. While constrained grids in the Mid-Atlantic and Midwest face rising utility costs and reliability crises, energy-rich markets like Texas and the Southeast are emerging as critical “safe harbors.”

For the market, this signals the end of stability and the beginning of deep volatility. As the grid strains under this massive infrastructure shift, power is ceasing to be a uniform commodity, it is becoming a scarce, location-specific asset where geography dictates survival.

Texas is emerging as a more stable environment for data center construction, particularly as the political climate intensifies during the midterm elections. The strategic distribution of sites and lower projected grid strain compared to other regions make infrastructure expansion in Texas less likely to become a focal point for political friction.

With gasoline prices climbing to $4.50 per gallon due to the ongoing conflict with Iran, electricity costs have become a critical factor for industrial operations. While this could be a point of tension, hyperscalers are expected to compensate for these costs to prevent any slowdown in construction.

Furthermore, companies are increasingly turning to alternative power solutions, such as on-site gas turbines, to ensure energy independence.

This shift is mirrored by industry leaders like MSFT 0.00%↑ who are prioritizing rapid data center expansion to meet demand, even if it means temporarily pivoting from previous green initiatives following recent earnings reports.

To manage public perception and avoid unnecessary scrutiny, there is a growing trend of anonymity in the sector. Crypto-miners-turned-infrastructure-providers are becoming increasingly secretive about their partnerships.

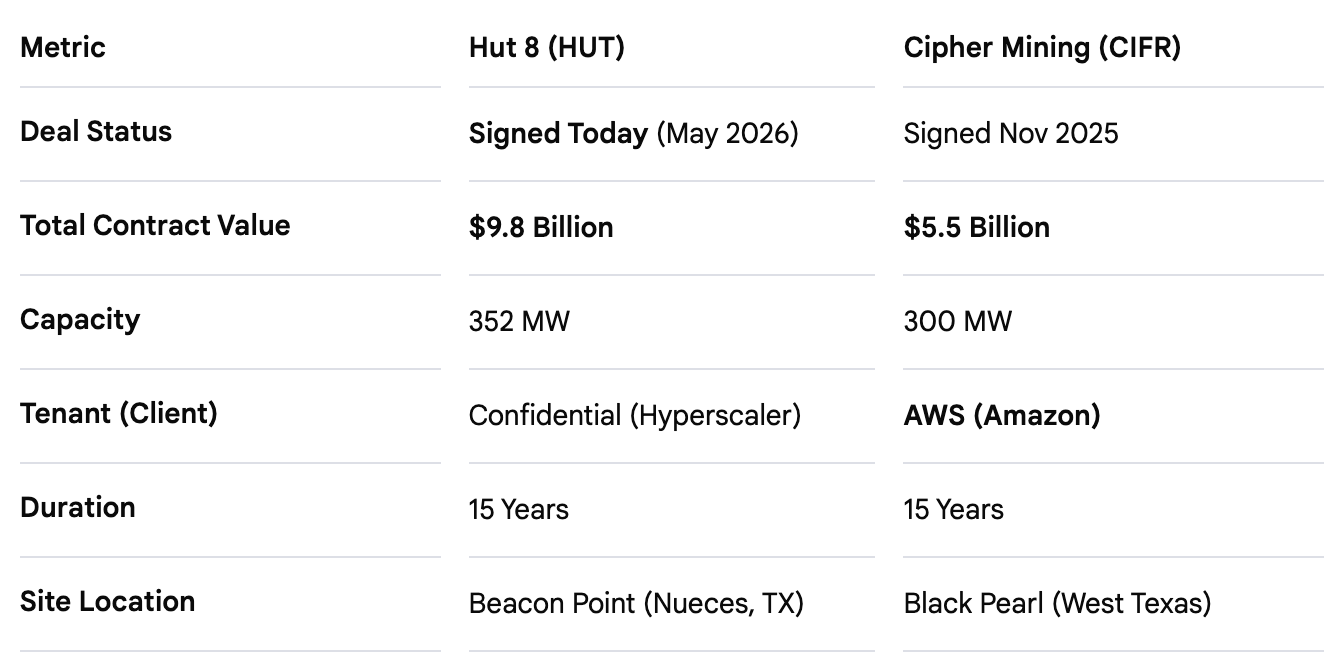

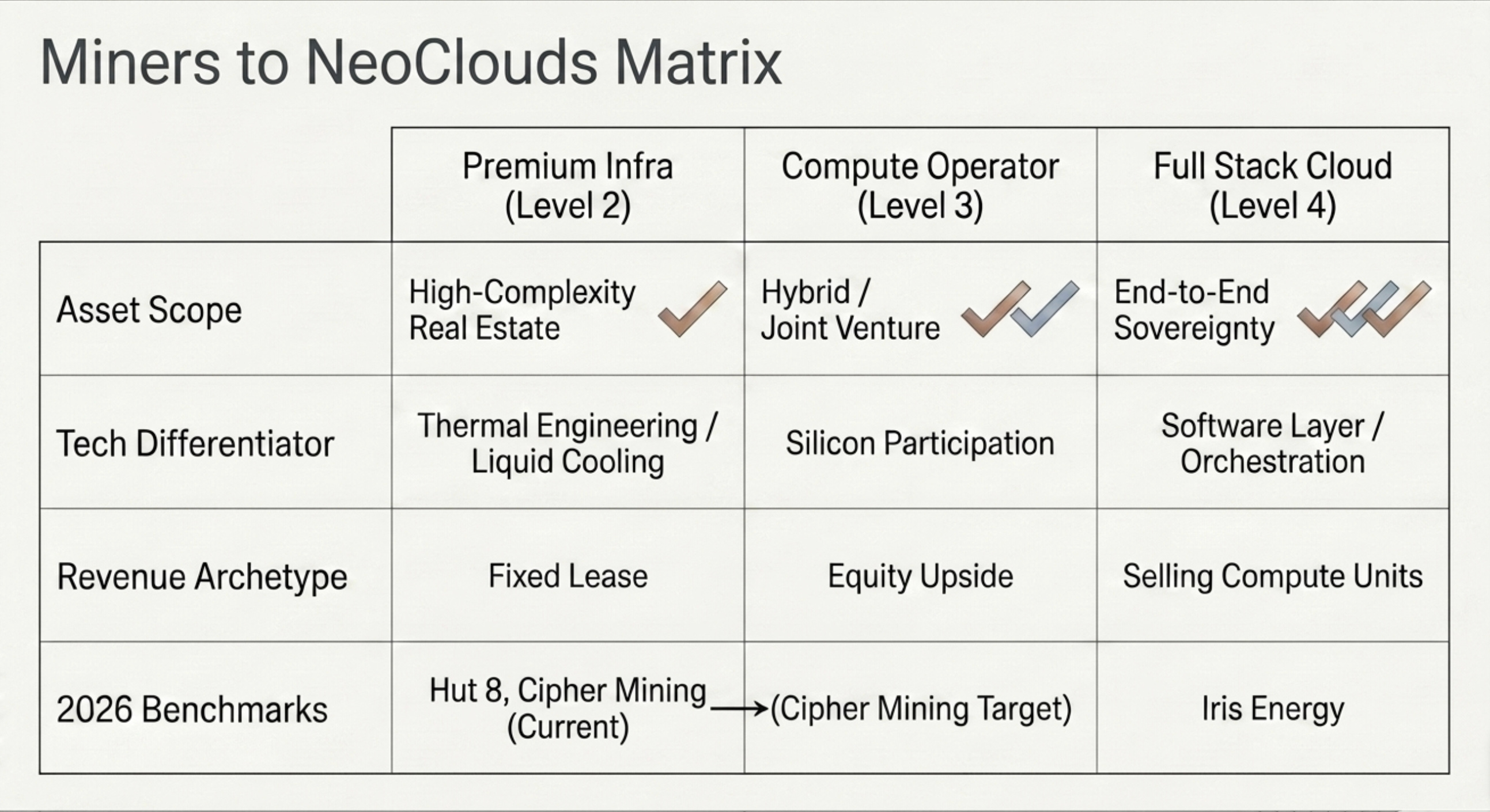

For instance, HUT 0.00%↑ and CIFR 0.00%↑ have recently secured major deals while keeping the identity of their clients undisclosed. I compared their deals to understand why the HUT 8’s agreement is so much more favorable.

When you strip away the press release marketing and look at the engineering physics, the premium Hut 8 secured is driven by three technical factors: the definition of usable power, the cost of Nvidia-specific infrastructure, and grid location.

1. The Trap: “Gross” vs. “Critical” IT Load

This is the single largest distortion in the comparison.

Cipher (CIFR): Their 300 MW figure is often cited as Total Site Capacity. In a traditional air-cooled facility (PUE ~1.25), a significant portion of that power runs fans and chillers. The actual power available for servers (IT Load) is likely closer to 240 MW.

Hut 8 (HUT): Today’s announcement explicitly specifies 352 MW of IT Load. This is “pure” power available for the chips, exclusive of cooling overhead.

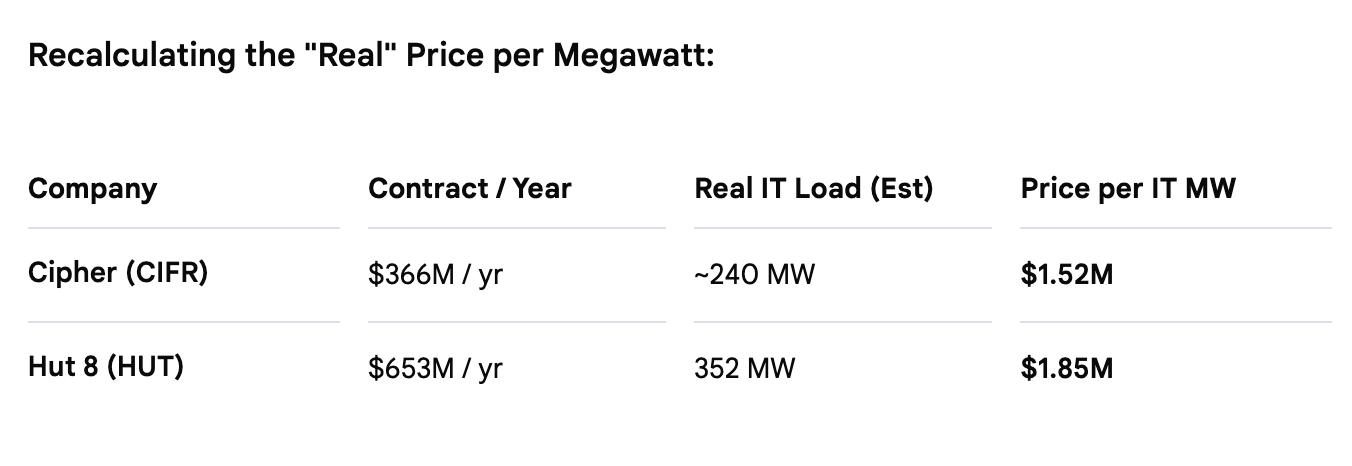

Result: The “premium” shrinks from ~50% to ~21%. This is a rational market increase, but there are still two other drivers.

2. The “Nvidia DSX” Factor (Capex Recovery)

Hut 8 isn’t just leasing a shell; they are effectively financing a custom factory.

Cipher: Built a standard Tier-3 shell. It’s efficient, but generic.

Hut 8: The deal explicitly mentions a redesign for NVIDIA DSX specifications. This requires high-density Direct Liquid Cooling (DLC) loops and reinforced floor loading for heavier racks (100kW+ per rack).

The Lease Logic: In a Triple-Net Lease, higher upfront construction costs result in higher monthly rent. Hut 8 spent more to build a “Ferrari” garage, so the tenant pays a higher lease rate than Cipher charges for a “Ford” garage.

3. Grid Physics: Congestion vs. Connectivity

The value of a megawatt in Texas depends entirely on where it sits on the ERCOT map.

⚡️ The “Grid Congestion” Tax

Cipher’s Black Pearl sits in the “West Zone,” an area famously known as a renewable energy bottleneck.

The Problem: The region generates more wind and solar power than the transmission lines can carry.

The Consequence: When lines are clogged, ERCOT forces users and generators to shut down (Curtailment) or prices crash to negative levels.

The AI Impact: Hyperscalers like AWS demand “five nines” (99.999%) reliability. They pay less rent in West Texas because they are effectively accepting a higher risk of grid instability and downtime.

🥶 The “Cooling Advantage”

Hut 8’s Beacon Point sits in Corpus Christi, a major industrial port.

The Advantage: Access to industrial-scale water infrastructure is critical for the next generation of AI. Nvidia’s Blackwell and Rubin chips require liquid cooling loops that are incredibly water-intensive.

The Premium: In the desert (Wink), water is a scarce luxury. On the coast (Corpus Christi), it is a utility. Hut 8 can support higher-density liquid cooling more cheaply and reliably than a desert facility, justifying the higher lease rate.

This imbalance has driven CIFR to conduct an experiment at a small site in Reveille, where they aim to become a co-owner of the compute—though the $700M on their balance sheet will admittedly not be enough for this. Nevertheless, we are seeing a clear differentiation among miners, and despite a 40% drop in U.S. data center construction, clients are demonstrating a willingness to pay a premium for quality.

IREN, for instance, was compelled to acquire Mirantis, although this move was obvious a year ago. Tomorrow, we will see the investors' reaction and find out when the next deal will take place.

This publication is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Readers are solely responsible for their own investment decisions. The author hold positions in IREN and CIFR