NVIDIA’s Robotics Push: The Stocks Worth Buying Right Now

The robotics market is set to hit $200B in the coming years. Here is where to find the future multibaggers right now.

While everyone is busy discussing chatbots and AI-generated images, the world is on the verge of a much bigger shift. Barclays predicts that the humanoid robot market will grow 100-fold over the next decade, clearing $200 billion. But honestly, these estimates are likely way too conservative. At some point, once the technology hits its stride, robots will start multiplying and flooding workplaces faster than AI can generate tokens.

There will be plenty of players in this race, but NVIDIA has already figured out how to make the most money. They are pulling off their signature move, the exact same playbook that made them the kings of computer graphics and deep learning.

The mechanics are simple: Developing a robot from scratch is brutally expensive and time-consuming. Every manufacturer has to spend years writing code just to teach a machine how to walk without falling over at the slightest push. NVIDIA stepped in and said: “Here is a ready-to-use operating system and baseline AI models. Take them and save your R&D money”.

As a result, robot makers - from American startups to Chinese giants - are happily adopting this software to skip billions of dollars in development costs. But the moment they do, they step right into the trap. Once the entire industry builds its applications on top of NVIDIA’s software, switching off it will be virtually impossible. NVIDIA will effectively become the main toll booth and infrastructure owner for the global robotics market.

The Bifurcated Market: China’s Hardware vs. Western Brains

The global robotics race isn’t going to have just one winner. Instead, the market is splitting into two completely different camps, each playing a totally different game.

Camp 1: China (The Kings of Cheap Hardware) China is treating humanoids exactly like they treated electric vehicles: push massive supplier ecosystems, cut production costs to the bone, and flood the market. Companies like Unitree are already selling robots for $10,000 to $13,500, the price of a cheap used car. They can do this because they are reusing China’s massive EV supply chain to stamp out motors and mechanical joints at lightning speed. The catch? On their own, these cheap robots lack advanced safety features and high-end processing power.

Camp 2: The West (The Kings of Complex AI and Safety) US and European giants like Tesla (Optimus) or Figure aren’t trying to build cheap toys. They are building expensive, vertically integrated machines designed to pass strict safety audits so they can legally work right next to human factory workers. They build their own custom actuators and proprietary AI brains, keeping tight control over the entire system.

NVIDIA’s Double Win

This market split is exactly why NVIDIA wins twice. They sit right in the middle of this geopolitical divide, collecting a toll from both sides:

Cheap Chinese hardware needs to get smart fast, so manufacturers plug Unitree’s low-cost bodies straight into NVIDIA’s Jetson onboard chips and GR00T software.

High-end Western developers need to test their custom setups without breaking million-dollar prototypes, so they use NVIDIA’s advanced simulators to train their models in a digital world before moving to the real factory floor

No matter who wins the battle for the physical robot body, NVIDIA owns the infrastructure powering it

Sourcing the Muscle: How NVIDIA Captured China’s Hardware Fleet

If you want to understand how this supercycle plays out on the global stage, ignore the political grandstanding about semiconductor bans. While Washington blocks NVIDIA’s top-tier data center GPUs from entering Beijing, NVIDIA has quietly executed a brilliant flank maneuver right through China’s robotics backdoor

They aren’t trying to sell high-end server chips to Chinese tech giants; they are shipping edge-compute brains (the Jetson Thor platform) and handing out software keys directly to China’s fastest-moving hardware startups.

Look no further than Unitree Robotics

China’s playbook for humanoids is an exact carbon copy of its electric vehicle strategy: exploit an ultra-dense, localized electromechanical supply chain to compress hardware costs to the absolute bone. Unitree shocked the industry by putting a public price tag of $10,000 to $13,500 on its G1 humanoid, the price of a cheap commuter car. They can pull this off because they sit in the middle of a massive manufacturing cluster, grabbing motors, bearings, and structural frames at fraction-of-a-cent margins.

But cheap hardware has a fatal flaw: it’s profoundly stupid. Left to their own devices, these dirt-cheap Chinese prototypes lack the complex vision systems, real-time balance, and basic safety guardrails required to step foot on an active assembly line without causing a disaster

Enter NVIDIA’s asymmetrical trade. They NVIDIA didn’t bother trying to build a cheaper mechanical body than the Chinese. Instead, they took Unitree’s H2 Plus chassis, loaded it with their high-performance Jetson AGX Thor T5000 board, and wrapped it in the GR00T cognitive software stack to create their official Reference Humanoid Robot.

The mechanics of this partnership are purely transactional:

For Unitree: They instantly wipe out billions in software R&D costs and skip years of trial-and-error by plugging into a world-class AI brain.

For NVIDIA: They ensure that the largest, fastest-scaling hardware fleet on earth is being built on their proprietary software architecture.

NVIDIA doesn’t care if geopolitical tensions freeze out traditional silicon markets. By partnering with Unitree and giving China the software tools to commoditize the robot body, NVIDIA guarantees that whenever a cheap Chinese robot walks out of a factory, it operates on an unskippable NVIDIA tax

The US Landscape: Real Capex, Pure Plays, and the Hidden Infrastructure Cash

While China focuses on scaling cheap hardware, the US ecosystem is where the heavy institutional capital is drawing the line between laboratory science fiction and actual corporate balance sheets. If you want to allocate capital here without getting burned by pre-revenue vaporware, you need to separate the asset classes.

1. The Logistics Overlords: Amazon and Tesla

Don’t buy Amazon (AMZN) or Tesla (TSLA) thinking they are “robotics startups.” They are the ultimate end-users and data collectors.

Take Amazon: they are committing over €10 billion to expand and upgrade their European fulfillment network with advanced automation. They aren’t waiting for a perfect human clone. They are deploying STARK, a dedicated robotic tote-handling system, across 15 European sites by 2027, and scaling Vulcan, a system built explicitly with the high-end tactile sensing capabilities that legacy automation lacks. Their upgraded Proteus autonomous floor robot doesn’t just sit in the loading docks anymore; it calculates its own routes, priorities, and timing across the entire warehouse floor. Amazon is building the structural demand; they are buying efficiency, not hype.

Tesla plays a similar game with Optimus, vertically integrating their automotive FSD compute stack into a custom bipedal frame to cut out third-party suppliers entirely. They are their own first customer.

2. Lidars: Ouster and Aeva

If you don’t want to guess whether Amazon’s or Tesla’s proprietary brain wins, you buy the eyes. You cannot move a multi-hundred-pound metal agent fenceless alongside human workers without flawless, low-latency 3D spatial awareness.

This is where the LiDAR plays become critical. OUST 0.00%↑ has already hardcoded themselves into NVIDIA’s ecosystem. Their new Rev8 digital LiDAR family runs on custom L4 Silicon featuring native-color fusion. By baking color data directly into the 3D point cloud at the chip level, they eliminate the clunky, power-hungry sensor-fusion software layers that drain robot batteries.

NVIDIA natively supports Rev8 inside their JetPack and Isaac ROS middleware, turning Ouster into a structural gatekeeper of physical AI perception.

AEVA 0.00%↑follows a similar high-assurance trajectory with FMCW technology, capturing velocity data along with depth.

3. The “Anti-Humanoid” Smart Money: Teradyne

Here is the ultimate institutional hedge. If you think humanoids are still too early, too clumsy, and too financially risky for mass adoption, you buy TER 0.00%↑ Teradyne owns Universal Robots (the undisputed global king of collaborative robotic arms, or cobots) and Mobile Industrial Robots (MiR) (autonomous warehouse vehicles). Teradyne doesn’t give a damn about building a robot that can walk up stairs or fold laundry. They care about factory throughput today.

While humanoid startups spend billions trying to figure out how to keep a bipedal robot from falling over when a battery dies, Teradyne’s stationary cobots and wheeled platforms are already generating billions in high-margin industrial revenue. They are the pragmatic alternative for investors who want automation capex without the humanoid execution risk.

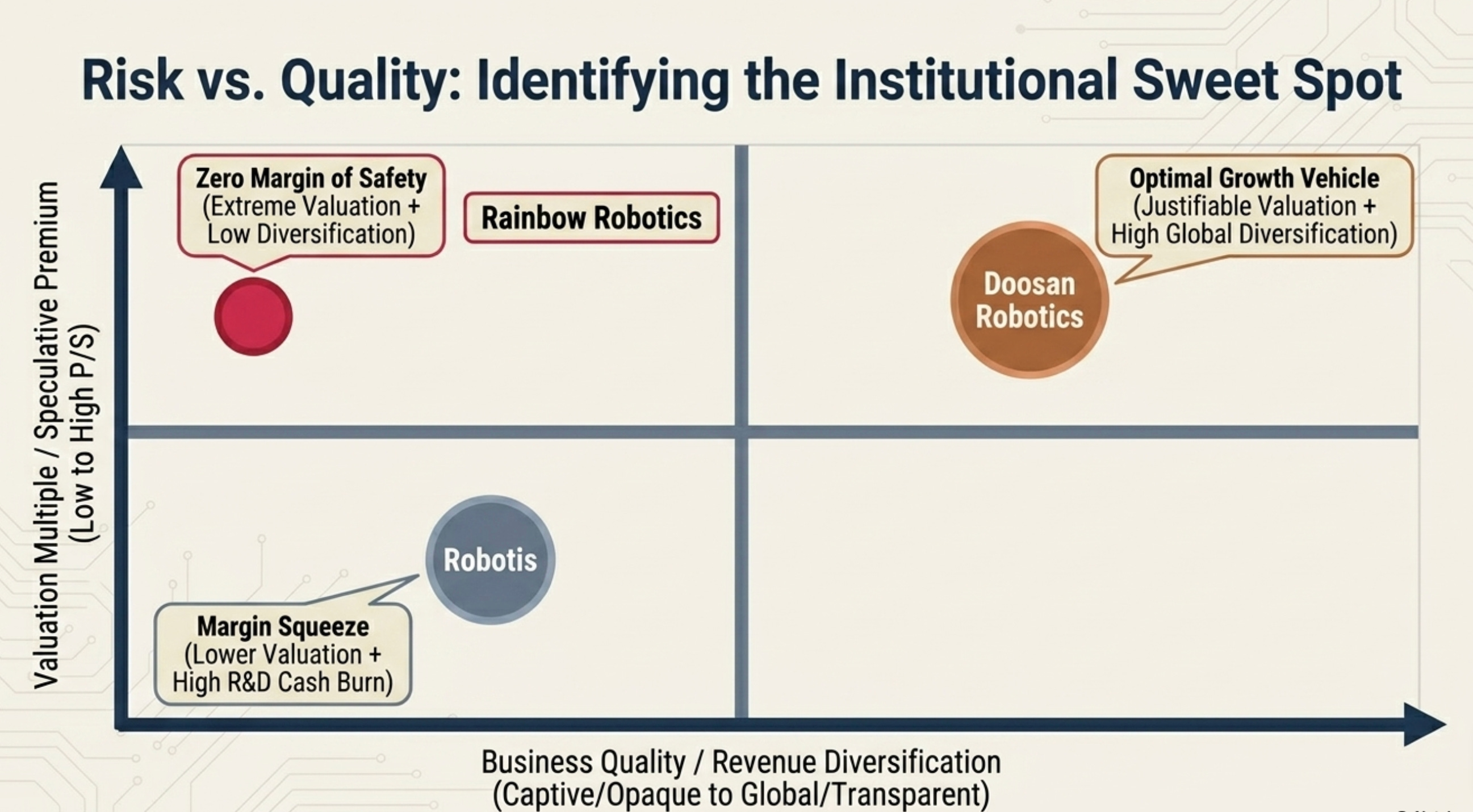

The South Korean Cluster: Industrial Execution vs. Valuation Traps

South Korea has become the explosive epicenter of the current Physical AI investment supercycle. When NVIDIA’s Jensen Huang visited Seoul, it triggered a massive rally across Korean robotics stocks on intense speculation over deep hardware-software cooperation. Retail investors are chasing anything with “robot” in the name, but if you look past the headlines and dive into the actual Q1 2026 financial balance sheets, the underlying realities of these companies could not be more different.

If you want to allocate capital in the Korean cluster without buying into pre-revenue vaporware, this is how you separate the actual winners from the valuation traps:

1. The Top Pick: Doosan Robotics (KS: 454910)

Doosan is the rare player successfully escaping “pilot purgatory” and transforming into a true global system integrator. They aren’t just selling bare-metal robotic arms; they are deploying complete, turn-key automated packaging cells straight into premium Western markets.

Following their acquisition of US automation firm ONExia, Doosan legally launched Doosan Robotics Americas, shifted its headquarters to Pennsylvania, and approved a new 90,000-square-foot facility to aggressively scale up North American production. The financial pivot is already visible on the tape: Doosan’s Q1 2026 revenue exploded by +189.7% year-over-year, driven by rapid US expansion and domestic automation demand.

The NVIDIA Connection: Doosan is a premier technological ally of NVIDIA. Their proprietary Agentic Robot OS officially embeds NVIDIA’s newly launched Cosmos 3, the open frontier foundation model for physical AI, alongside the cuMotion path-planning library. This enables their collaborative robots to dynamically recognize obstacles, read product labels, and instantly calculate motion paths on a live production line without any manual programming.

Yes, they are still reporting a temporary operational loss due to aggressive front-loaded investments in AI developers and US hiring, but with a massive post-IPO cash cushion of 245 billion won and practically zero debt, Doosan is the cleanest commercial execution play in Asia.

2. The Valuation Trap: Rainbow Robotics (KOSDAQ: 277810)

On paper, Rainbow Robotics looks like an institutional darling. Samsung Electronics recently executed its options to push its stake to 35%, effectively absorbing the company into its corporate контур and turning it into a captive, in-house automation provider for Samsung’s semiconductor fabs, logistics hubs, and shipyards. Backed by Samsung’s massive volume, their Q1 2026 revenue jumped a solid +117%.

But look at the actual market math. Rainbow is currently trading at a jaw-dropping, completely detached 380x to 540x LTM Price-to-Sales. You are paying for roughly 500 years of current revenue today. Their entire growth trajectory is trapped inside the capital expenditure budget of a single customer.

To make matters worse, the stock is carrying severe corporate governance risks: Seoul prosecutors recently raided their headquarters over an insider trading probe, alleging that management used non-public info about the Samsung buyout to front-run the stock for illicit profits. At these extreme multiples, with toxic legal clouds overhead, you stay far away.

3. The R&D Money Pit: Robotis (KOSDAQ: 108490)

Robotis occupies a highly critical infrastructure niche. They manufacture DYNAMIXEL smart actuators, the highly precise mechanical “joints” that other companies buy to make their humanoids and robotic arms move. LG Electronics is a major strategic backer, securing a steady component sales channel.

The problem? Robotis is trapped in a brutal, capital-destroying R&D arms race. Their Q1 2026 earnings revealed a catastrophic consolidated operational loss of 11.84 billion won on flat revenues. Why? Because they had to nearly quadruple their quarterly R&D spending to 9.42 billion won just to upgrade their actuator tech and prevent aggressive, lower-cost Chinese component makers from eating their market share. Robotis has to burn almost every dollar it makes just to stand still, historically resulting in negative returns on equity and constant shareholder dilution. They are a vital supplier, but a terrible vehicle for generating free cash flow.

4. The Micro-Cap Alternative: SBB Tech (KOSDAQ: 389500)

If you want to hedge against the near-monopoly of Japanese gearbox makers like Harmonic Drive, SBB Tech is South Korea’s homegrown alternative. They specialize in localizing the manufacturing of precision bearings and harmonic reducers, aiming to dramatically slash component costs for domestic robot makers. It’s a high-risk, micro-cap bet on supply chain independence, but if they can capture even a fraction of the market pivoting away from high Japanese hardware premiums, the upside is highly asymmetric.

Crucially, SBB Tech supplies harmonic reducers and actuators directly to Hyundai for their Robotics Lab and smart manufacturing platforms. This puts SBB Tech in a highly strategic position: Hyundai happens to own Boston Dynamics, widely recognized as the most advanced humanoid robotics company on the planet. By embedding its hardware into Hyundai's automation and R&D pipelines, SBB Tech acts as a high-risk, asymmetric micro-cap play on domestic supply chain independence. If they can capture even a fraction of the hardware volume moving through Hyundai's massive industrial ecosystem, the upside is massive.

The Japanese Throttle: Hardware Monopolies

If you want to move away from the software layers and the corporate end-users, you have to look at the cold, hard laws of physics. The single largest cost block of any humanoid robot is actuation, the motors and gearboxes that allow joints to move, accounting for a staggering 40% to 60% of the entire bill of materials.

You can write the most brilliant AI software in Silicon Valley, but if your robot doesn’t have a high-torque, precision gearbox in its knee or elbow, it’s just a very expensive, motionless metal statue. And when it comes to precision mechanical joints, Japan owns the entire global infrastructure.

If you want a pure-play investment on the literal nuts and bolts of this industry, you look at two companies:

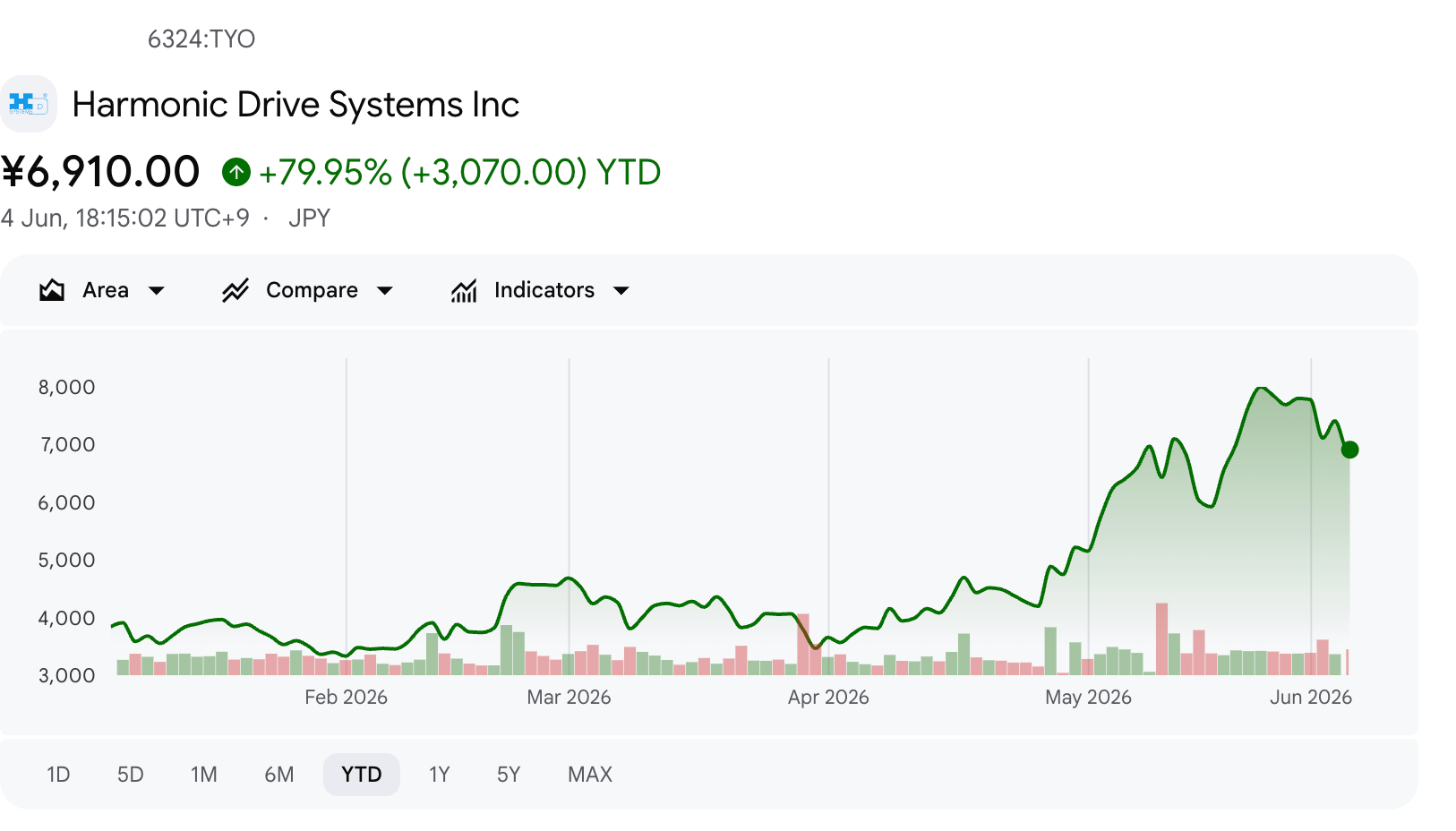

1. Harmonic Drive Systems (Tokyo: 6324)

This is the ultimate bottleneck asset. Humanoid joints require incredibly compact, light, and zero-backlash gearboxes. The industry standard for this is the strain-wave drive, and Harmonic Drive Systems is the undisputed, historical gatekeeper of this technology.

Scaling up production for these gearboxes is capital-intensive, precision-bound, and requires long qualification cycles. Unlike software, you cannot just spin up more server capacity to build a gearbox; it requires heavy industrial machinery and decades of metrology expertise. As every humanoid maker tries to scale production from dozens of pilots to thousands of commercial units, they all rush to the exact same Japanese doorstep. It is a structural choke point.

2. Nabtesco Corporation (Tokyo: 6268)

While Harmonic Drive dominates the micro-precision joints like wrists and fingers, Nabtesco is the king of heavy lifting. They specialize in cycloidal drives, which are preferred for larger, high-impact robotic joints that require extreme durability and torque density like hips and knees.

If a robot falls over, backdriving forces can instantly shatter a cheap gearbox. Nabtesco’s cycloidal setups are built to survive industrial factory floors. While alternative gearbox tech exists, Nabtesco remains deeply insulated from competition due to massive barriers to entry in precision engineering.

While the US and China fight a loud geopolitical war over AI models and software standards, Japanese component suppliers are quietly sitting back, waiting to collect their hardware tax from every single robot that gets assembled anywhere on Earth.

Many of these companies have already seen significant runs, but they still hold massive upside as the broader market scales. Because of this, the smart play is to build your positions gradually, especially since pre-profit tech stocks are notoriously volatile. By diversifying your exposure, buying both the final robot manufacturers and the core actuator component suppliers, you can significantly de-risk your portfolio.

Personally, I see a very strong combination in pairing Hyundai with Doosan Robotics, though I am still patiently waiting for a cleaner entry point on Doosan before pulling the trigger.

This publication is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Readers are solely responsible for their own investment decisions. The author hold positions in Hyundai and NVIDIA

Great read

$APH for picks and shovels