Will Doosan Robotics Do to the Sector What NVIDIA Did to AI?

A surging stock price leaves investors with a critical question: wait for a pullback or start building a position?

According to KB Securities, the humanoid market is projected to grow at a CAGR of 77% (2026–2035), expanding from $4B to $663B.

Naturally, everyone wants a piece of this growth. But if you look at the US public markets, direct pure-play options are extremely limited. Investors are mostly left with foundational enablers like NVDA 0.00%↑ or hardware infrastructure proxies like lidar manufacturers OUST 0.00%↑. The prominent humanoid startups are either still private like Figure or tucked away inside massive tech conglomerates

South Korea offers a fundamentally different dynamic. The local ecosystem features pure-play robotics companies that are already publicly traded, allowing investors to gain direct exposure through the open market.

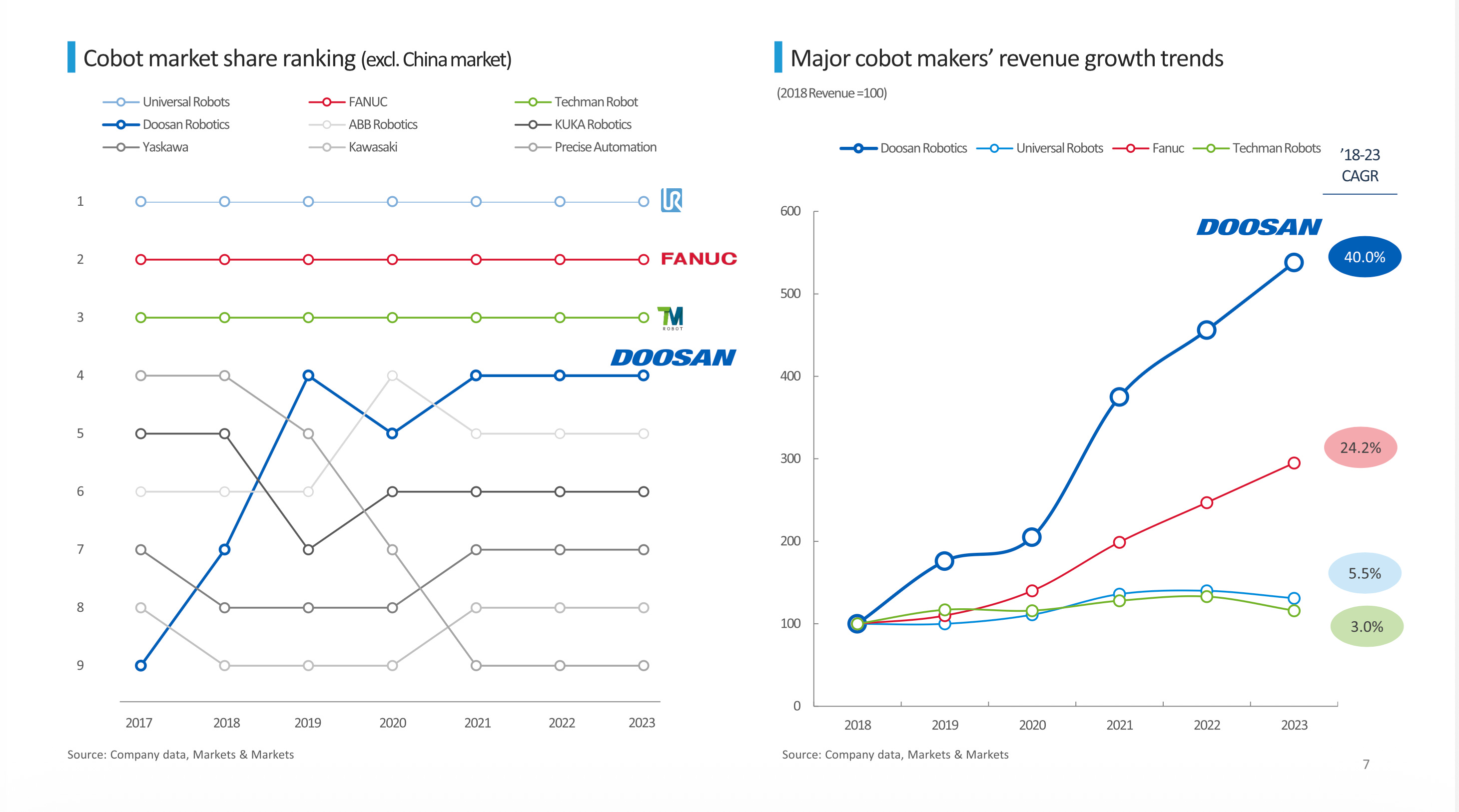

At the center of this landscape is Doosan Robotics (KRX: 454910).

The company represents a compelling case study in structural business model transformation. While traditional financial frameworks often flag its consecutive years of net deficits, forward-looking market participants are focusing on its shift from an industrial hardware vendor to a high-margin “Physical AI” software platform.

The Family

Doosan Robotics is already a top-5 global player in collaborative robots (cobots). They have established manufacturing facilities, a global distribution footprint, and active commercial contracts.

In Q1 2026, the company reported a 189.7% year-over-year revenue surge. While operating margins remain negative due to aggressive R&D and expansion costs, the underlying volume is scaling rapidly, driven by U.S. commercial backlog and the integration of their newly acquired systems integrator, ONExia.

Right now, Doosan is undergoing a radical transition into software-defined automation. Their proprietary Dart-Suite ecosystem moves the business toward no-code, drag-and-drop AI task planning, drastically lowering integration costs for end-users. At CES 2026, their vision-based AI solutions earned top innovation awards, showcasing machines that adapt to unmapped environments in real time without pre-defined CAD data.

This software-defined foundation serves as their direct springboard into humanoids. Doosan Robotics has officially established a product roadmap targeting the commercial launch of industrial humanoid platforms by 2028. They are executing this strategy as a core member of South Korea’s state-backed K-Humanoid Alliance, while simultaneously collaborating with Nvidia to train their models via the Isaac Sim pipeline and co-developing custom on-device AI semiconductors.

Ultimately, Doosan offers a unique equity vehicle: a business with a proven hardware moat, zero debt, a 6-year cash runway, and an embedded call option on the physical AI revolution.

We will break down the mechanics of their balance sheet, the strategic importance of their U.S. footprint, the structural impact of their recent corporate restructuring, and how they stack up against global peers like Universal Robots and Fanuc.

To evaluate Doosan Robotics properly, it must be viewed through the lens of its corporate architecture. The company functions as the high-tech vanguard of the Doosan Group, one of South Korea’s oldest and most deeply capitalized chaebols (conglomerates).

Established in 1896, Doosan Group has pivoted across multiple industrial cycles over the last century. Today, the conglomerate generates between $13B and $15B in annual revenue, commanding structural market positions in heavy infrastructure, nuclear power components, clean energy, and semiconductor testing. When an industrial parent of this scale establishes a dedicated robotics division, the investment horizon is measured in decades, backed by significant corporate treasury and deep engineering synergies.

The structural origin of Doosan Robotics began in July 2015. Faced with accelerating demographic headwinds and labor shortages across industrial economies, particularly in East Asia, Doosan Group formed the subsidiary to capture the shifting economics of factory automation.

Cobots

Rather than entering the highly commoditized market for traditional, high-payload industrial robots that operate in isolated safety cages, Doosan focused its initial three-year R&D cycle entirely on collaborative robots. The primary technical objective was mastering force control; the company developed and standardized high-precision torque sensors across all six joints of its robotic arms, a feature typically omitted by lower-cost competitors.