Robinhood ($HOOD): The Yass-Trump Triangle. Why the "King of Market Makers" is the Secret Architect of the Next Retail Surge

Unpacking the PFOF Dependency, the TikTok Lobby, and the Political Shield Protecting the House of Retail.

The market reassessed HOOD 0.00%↑ the moment BTC hit its historical maximum and entered a phase of turbulence. While the stock climbed on the enthusiasm of the past year, many investors, myself included, fell into a classic trap: Anchoring Bias.

We often evaluate an asset’s potential by looking at its past peaks, subconsciously believing the price is “obligated” to return to those levels. But in investing, it is not where the price was that matters, but rather the factors driving it now.

From Favorites to Pariahs

In the market, there is a concept of a company changing its “state of matter.”

Phase of Incredible Strength: This is what we are currently seeing in the semiconductor sector (AMD, ARM). The market forgives any degree of overvaluation because it believes in exponential growth.

Phase of the Market Pariah: As soon as a business model shows a crack, the asset instantly loses its status. Today’s 8% drop in META is a prime example; the market wasn’t just looking for good numbers, it expected perfection. When a company ramps up CapEx on AI without an immediate return, investors slam on the brakes.

As Benjamin Graham famously said:

“In the short run, the market is a voting machine, but in the long run, it is a weighing machine.”

Today, the “scales” are weighing against Robinhood, and one must have the courage to recognize that.

Robinhood’s 15% revenue growth in Q1 2026 looks weak against the industry average of 21% and the company’s own past performance of 50%+. Total revenue reached $1.07 billion, falling short of the projected $1.13–$1.17 billion.

The primary weight on these numbers was the crypto revenue crash: cryptocurrency transaction revenue plummeted 47% year-over-year to $134 million as trading volumes dried up.

The company is now facing a classic Innovator’s Dilemma. The very features that built its empire - commission-free trading and crypto speculation - are now dragging HOOD down. Meanwhile, new initiatives like prediction markets haven’t gained enough traction to compensate for the decline in core speculative revenue.

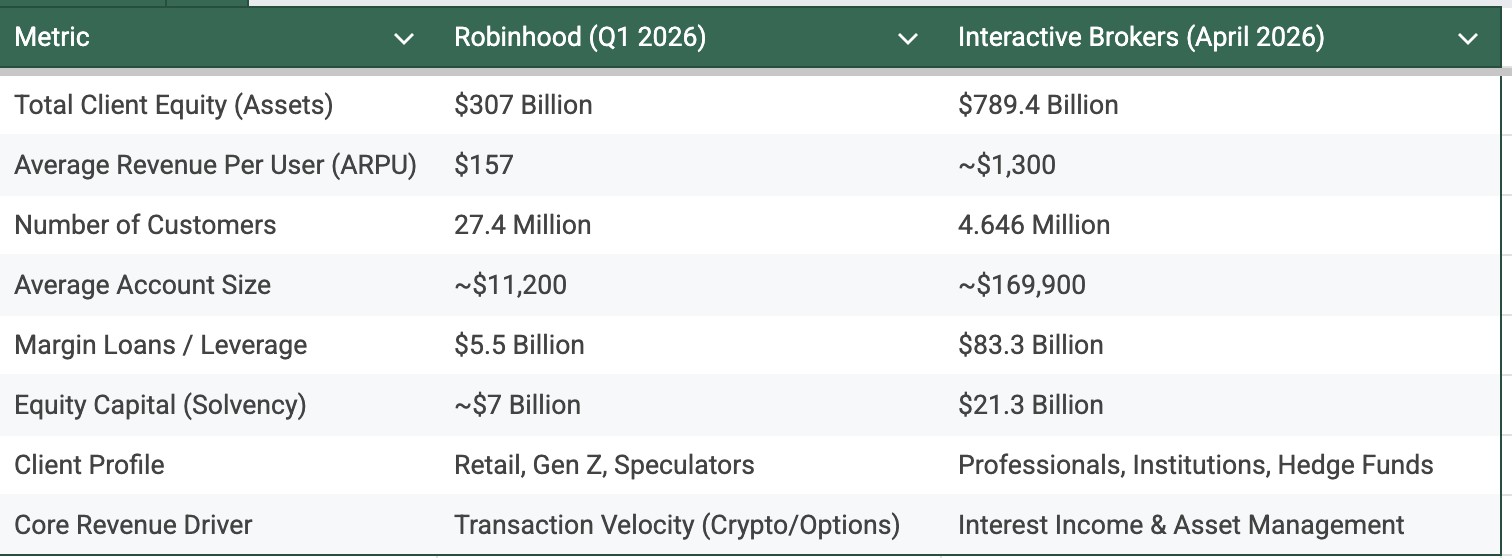

The Fundamental Gap: Why HOOD is Not IBKR

If you strip away the hype and look at the raw numbers, you see a chasm in business quality. Robinhood’s “commission-free trading” model is a double-edged sword.

Structural Comparison: Robinhood (HOOD) vs. Interactive Brokers (IBKR)

The 8x income gap is explained by the quality of the audience. During drawdowns, retail players, Robinhood’s core base, are the first to exit the market. This is why a stock bought at $70 requires significantly more time to recover: it doesn’t just need to “grow,” it needs to reinvent its profitability in a high-interest-rate environment.

The company is not standing still. During the earnings call, Tenev announced a record-breaking April. They are also partnering with Susquehanna (SIG) to launch Rothera, a dedicated platform for prediction markets. We will return to this partnership later. However, Robinhood’s primary source of pride isn’t just innovation- it’s traditional banking products.

Instead of calling it “copying JP Morgan,” they label it as building a “Super-App”.

The Super-App Strategy by the Numbers:

Retirement Accounts: Assets Under Custody (AUC) grew 90% YoY to $27.4 billion. This represents a fundamental shift from “speculative” capital to long-term assets.

Gold Ecosystem: The number of subscribers increased by 36% to 4.34 million. Gold users hold 5 times more assets than regular users, creating a stable financial foundation.

Lending: Gold Card balances surged 400% to $1.1 billion. Robinhood is effectively converting traders into long-term borrowers.

Banking Status: 40% of active customers now use Direct Deposit. The platform is becoming a primary place for storing salaries rather than just an “app for stocks”.

Historical Parallels: Cisco and the 2000s Trap

History teaches us that great companies can go years without returning to their peaks.

In March 2000, Cisco was the most valuable company in the world at $80 per share.

It was a magnificent company that was literally “building the internet.”

Despite Cisco’s business continuing to grow for decades, the stock only returned to those levels 20 years later.

The problem wasn’t that Cisco was a bad company. The problem was that in 2000, investors paid a price that priced in 100 years of future growth. The situation with the SaaS sector and Robinhood today shares these traits: the market overestimated their “bright future,” and now the hangover has arrived.

This is where Robinhood demonstrated an agility that few can match, revealing the Edge we are reporting on first. We spent a long time trying to understand why Robinhood specifically secured millions of American accounts under the Trump program.

The answer likely lies in the connection with Susquehanna (SIG), their partner for prediction markets. The head of Susquehanna, Jeff Yass, is a longtime associate of Trump and a major donor to the Republican Party. Furthermore, as a co-owner of TikTok, Yass was instrumental in helping the platform avoid a ban.

When you connect these dots, it becomes clear why Robinhood specifically received Trump’s backing. The $100 million invested in a platform for these users is a small price to pay, one that is poised to yield a massive, multi-fold return on investment.

The “Trump Accounts” program is a massive government-scale contract targeting 60 million potential users. To put this in perspective, this is more than double Robinhood’s current client base of 27.4 million.

Scale and Acquisition Challenges

Acquiring an audience of this magnitude through standard methods is nearly impossible for several reasons:

Customer Acquisition Cost (CAC): In the fintech industry, acquiring one active client typically costs between $50 and $100. For 60 million people, this would require a marketing budget of $3–$6 billion, which is comparable to the company’s entire annual revenue.

Administrative Leverage: This program grants Robinhood direct access to users through government mechanisms, effectively bypassing market competition with giants like Schwab or Fidelity.

Infrastructural Challenge: Robinhood has allocated $100 million to develop the platform for this influx. In the context of acquiring millions of users, this is a bargain, as the CAC within this program drops to a record low of approximately $1.60.

The Susquehanna and Jeff Yass Connection

As noted, the key Edge here is political capital:

Jeff Yass (Susquehanna) is more than just a partner for the Rothera platform. He is one of the largest Republican donors and has direct access to Trump.

His success in lobbying for TikTok (where he holds a significant stake) proves his ability to navigate national legislation.

For Robinhood, this partnership served as the “entry ticket” to a program that allows them to skip decades of organic growth

Economic Impact

If Robinhood successfully converts even 20–30% of these 60 million into active users:

Assets Under Custody (AUC): Even with an average account of $5,000 (lower than the current $11,200), it would add $60–$90 billion to client capital.

ARPU Arbitrage: At the current revenue per user of $157, this mass of users would allow the company to finally break through its revenue ceiling and justify a “Super-App” valuation.

This program is the strategic lever that transforms Robinhood from a “meme” app into a systemically important financial institution, tightly woven into the U.S. political elite.

Strategy: Opportunity Cost

But all of that is about future prospects; an investor is interested in a simple question: what do you do right now, when CAT 0.00%↑ is up 10% and you are just sitting there waiting for crypto to break $80K?

An investor’s greatest mistake is turning from a trader into a “forced long-term investor” simply because a position went into the red.

George Soros once said:

“It’s not whether you’re right or wrong that’s important, but how much money you make when you’re right and how much you lose when you’re wrong.”

If your capital is frozen in a stock that will take years to recover, you are committing a crime against your own portfolio. That money could be working in sectors showing “incredible strength,” such as Big Tech or semiconductor, there are many opportunities in the market

To act like a professional, answer these three questions:

The “Clean Slate” Test: If you didn’t have a position in Robinhood today, would you buy it at the current price for the same amount? If the answer is “no,” you are holding it only because of an emotional attachment to your loss.

Margin/Leverage Assessment: If you are being squeezed by options or margin requirements, cut the position immediately. Time is working against you (Theta decay).

The Reallocation Horizon: Set a deadline (e.g., 3 months). If the earnings reports don’t show an explosive growth in ARPU by then, reallocate into alternative instruments.

Sometimes the best strategy is inaction. But that inaction must be a conscious calculation, not paralysis. Always remember: the market doesn’t know what price you bought at. It doesn’t care. Your task is not to “get your money back,” but to earn new profit.

If you believe in Vlad Tenev, who has saved the company once before, then the stock is worth holding without dwelling on the fact that it once traded at $150. This might even be a good opportunity to average down your position. However, you must realize that if crypto takes a downturn and investors shift their focus toward AI stocks, this could become a quarter of missed opportunities. Personally, I’m not selling yet; I’ll monitor the price action, as my cost basis allows me to stay in the game.

This publication is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Readers are solely responsible for their own investment decisions. The author holds a position in HOOD