ServiceNow ($NOW): When Organic Growth Slips Below 20% and AI Can’t Close the Gap (Yet)

Unmasking the 19% Organic Growth Reality, the SBC "Tax," and the $7.75B Struggle to Keep the SaaS Dream Alive

Today, NOW 0.00%↑ shares plunged 17%, retreating to levels not seen since late 2022. On the surface, the headline numbers looked solid: a beat on top and bottom lines, raised guidance, and a narrative centered on AI. But the market isn’t buying the “growth at any cost” story anymore. Here is why this crash is a wake-up call for the entire software sector.

The Illusion of Acceleration: A Currency Mirage

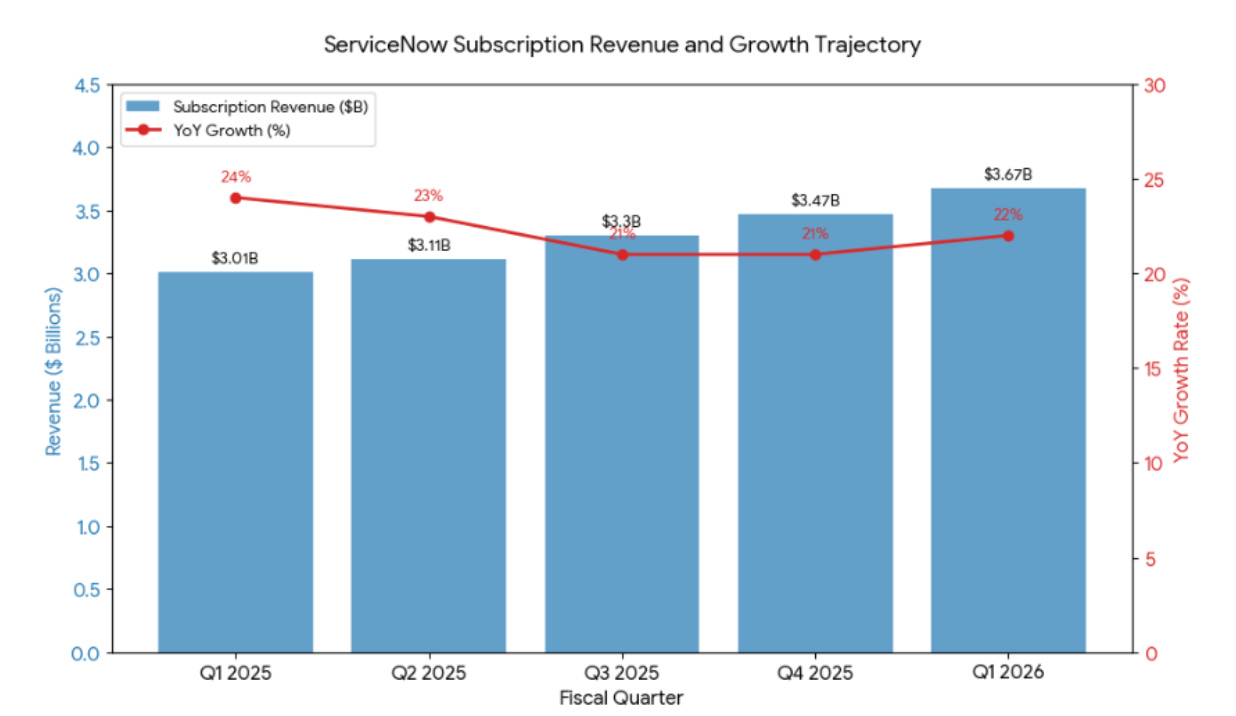

ServiceNow reported subscription revenue growth of 22% for Q1 2026. While this looks like an acceleration from the 21% seen in the previous quarter, the investor presentation reveals a different reality.

The company benefited from a massive 300 basis point (3%) currency tailwind. Without this FX gift, organic growth in constant currency actually slowed to 19%. For a company priced for “forever growth,” slipping below the 20% mark, once you strip away the exchange rate fluctuations, is a psychological breaking point for institutional investors.

Buying Growth: The $7.75 Billion “Armis” Tax

The most jarring detail was the acquisition of Armis for $7.75 billion in cash. This is a defensive move of massive proportions. Management admitted that Armis (and new AI capabilities) will contribute roughly 125 basis points to the full-year growth.

Essentially, ServiceNow is “buying” its growth numbers to keep them above 20%. But this growth comes at a steep price:

Operating Margin: Integration is expected to drag margins down by 75 bps.

Free Cash Flow: FCF margin is hit by 200 bps.

Q2 Outlook: Operating margins are projected to drop to 26.5%, a significant decline year-over-year.

The “Devil in the Details”: The SBC Racket

While a forward non-GAAP P/E of 24x after 70x+ might seem to align with industry standards, the devil, as they say, is in the details. The company spent $570 million on Share-Based Compensation (SBC) this quarter alone. Essentially, every sixth dollar earned goes toward employee bonuses. That’s roughly $2 billion a year.

It is important to realize that if these metrics were not constantly sanitized via non-GAAP adjustments, adjustments that exclude these massive SBC costs, the valuation multiples would not look reasonable. They would still look exceptionally bloated.

And when the company touts “share buybacks,” they aren’t returning value to shareholders, they are merely reducing the number of shares in circulation because they had to print new shares for SBC.

In the past, when revenue grew at 25%+, investors turned a blind eye to this dilution. Those days are over. Companies will now have to slash SBC or conduct massive layoffs, as Oracle has already done. This “shareholder tax” must end, or be paid in actual cash, which would further tank FCF.

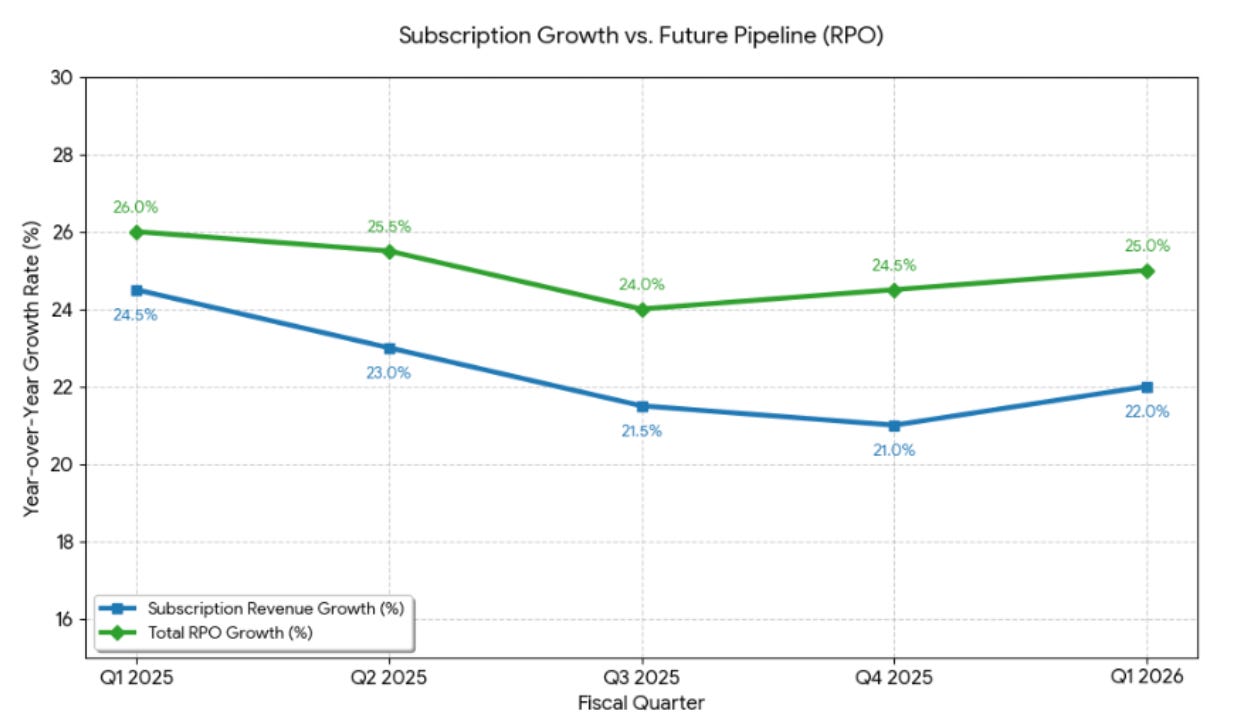

The RPO Paradox

One “bright” spot was the Remaining Performance Obligations (RPO), which reached $27.7 billion. However, even this was distorted by 200 bps of currency tailwinds. Furthermore, the company admitted to a 75 bps headwind from deal delays in the Middle East. When a giant like ServiceNow starts citing geopolitical “deal delays,” it usually suggests that the sales cycle for expensive SaaS is lengthening across the board.

The New Reality: Multiple Compression and the IBM Warning

We are witnessing a structural shift. Analysts are no longer slapping 50x multiples on SaaS companies just because they grow at 20%. The emergence of OpenAI and Anthropic - who are already reporting revenues that rival established leaders - has changed the game.

If you want to see the terminal stage of this lack of focus, look no further than IBM. It stands as the most egregious example of corporate inefficiency in the sector. Growing at a pathetic 4-5% a year, IBM 0.00%↑ is a “zombie” weighed down by a bloated consulting arm that acts as a structural anchor. They have failed to define a clear “moat” in the AI era, and their existence serves only as a cautionary tale: this is what happens when a tech leader stops innovating and starts merely “managing decline.”

Unless companies like ServiceNow undergo radical transformation, cutting bloated SBC and trimming the fat, they risk following the same path.

Bottom-fishing in SaaS remains a low-probability trade. The threat from LLM-native competitors is far from exhausted, and I prefer sectors with superior structural clarity. For now, I’m staying on the sidelines

This publication is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Readers are solely responsible for their own investment decisions. The author may hold positions in the securities mentioned.

And GAAP EPS of $0.45 vs $0.44 … made up numbers?