The death of cyclicality and rise of humanoids: what Micron's ($MU) earnings tell us about memory

Micron just transformed into an infrastructure monopoly, funded by its own desperate customers and ready to power the physical AI revolution.

Micron’s fiscal Q3 2026 financial results represent a monumental paradigm shift. This isn’t just another “beat and raise” quarter; it is the official funeral of the old, highly volatile semiconductor memory business model.

Historically, commodity memory chipmakers operated under a brutal boom-and-bust dynamic: a supply deficit triggered an exponential price spike, leading to industry-wide overproduction, followed by an immediate price collapse and devastating net losses.

That era is contractually dead. Artificial intelligence has fundamentally elevated advanced memory into a scarce, tightly allocated strategic infrastructure asset.

Structural Transformation: The “Take-or-Pay” Fortress

The core thesis of this report lies in the introduction of Strategic Customer Agreements (SCAs). To guarantee their hardware roadmaps for the next five years, hyperscalers and tier-1 customers are transferring immense balance sheet risk back to Micron.

Volume Lock-In: Micron has finalized 16 SCAs spanning the data center, automotive, and consumer segments. These binding contracts lock up roughly 20% of Micron’s total DRAM volume and one-third (33%) of its NAND volume from calendar 2026 through the end of 2030.

Contractual Price Floors: The largest agreements utilize a “floor and ceiling” pricing architecture. Crucially, management confirmed that the guaranteed gross margins at these contractual floor prices are locked well above the peak quarterly margins of any past cycle.

AI has elevated the value of memory. Micron is collaborating closely with our customers and suppliers across technology, product, manufacturing, and commercial teams in this tight industry environment. Strategic customer agreements are ushering in an exciting era for Micron. We expect these SCAs to significantly enhance the durability and predictability of Micron's strong financial performance, accelerating the transformation of our business model. Sanjay Mehrotra, CEO

The $100 Billion Baseline: 14 of the 16 signed agreements guarantee a staggering cumulative revenue floor of approximately $100 billion over the remaining contract terms.

$18B Interest-Free Financing: To secure these allocations, customers are handing over $22 billion in cash deposits and financial commitments, with roughly $18 billion delivered in raw, unrestricted upfront cash. This massive capital injection structurally funds Micron’s aggressive multi-billion dollar capex expansions without diluting shareholders.

Customers are so terrified of an absolute HBM shortage in 2027–2028 that they are willingly acting as Micron’s interest-free infrastructure financiers.

Beat and Raise

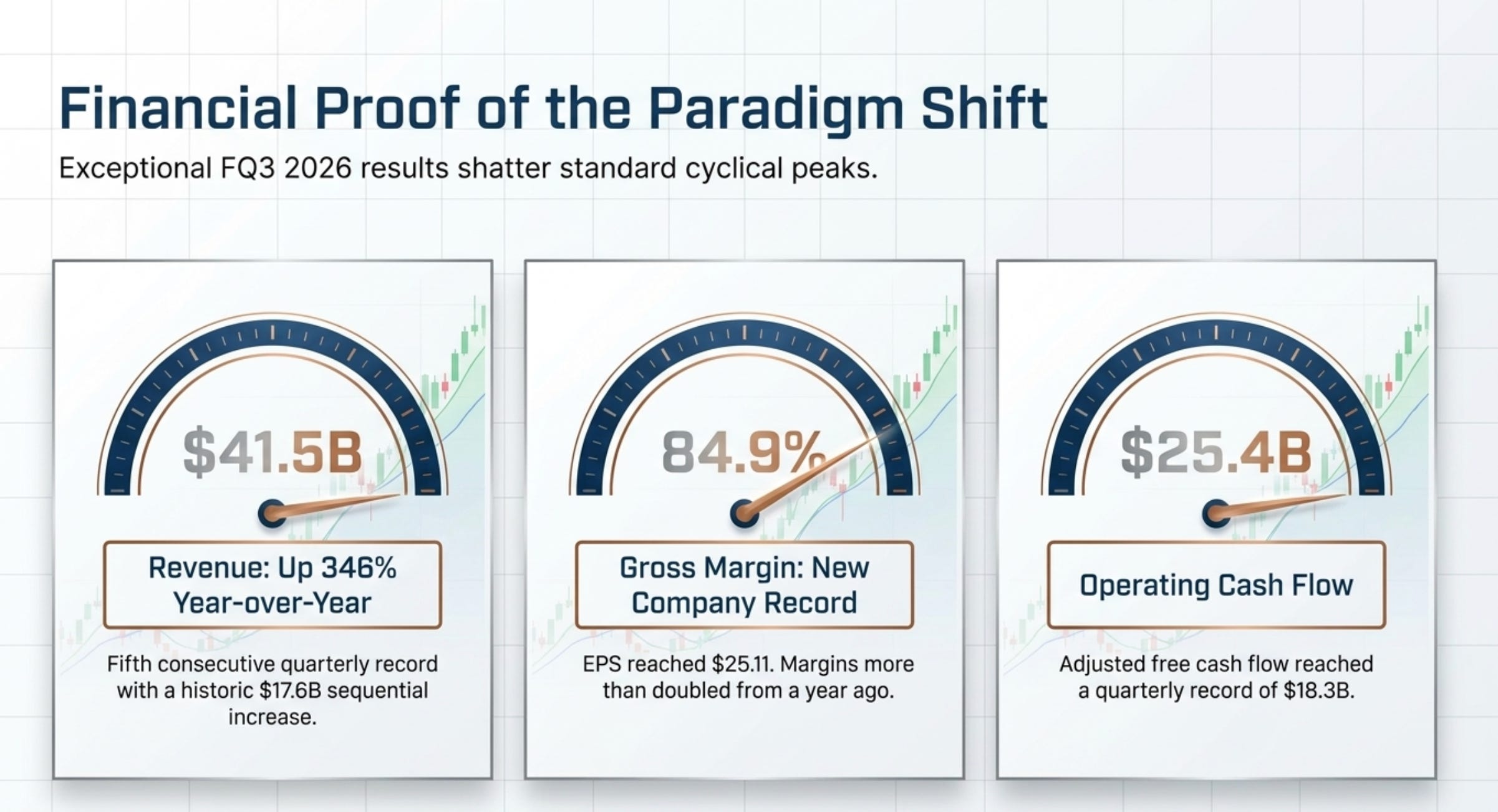

Revenue: $41.46 billion, marking an explosive 74% sequential jump and a 346% increase year-over-year.

Non-GAAP Gross Margin: Rocketed to an unprecedented 84.9%.

Non-GAAP Operating Income: $33.68 billion , reflecting a massive 81.2% operating margin.

Adjusted Free Cash Flow (FCF): A record-shattering $18.3 billion in a single quarter.

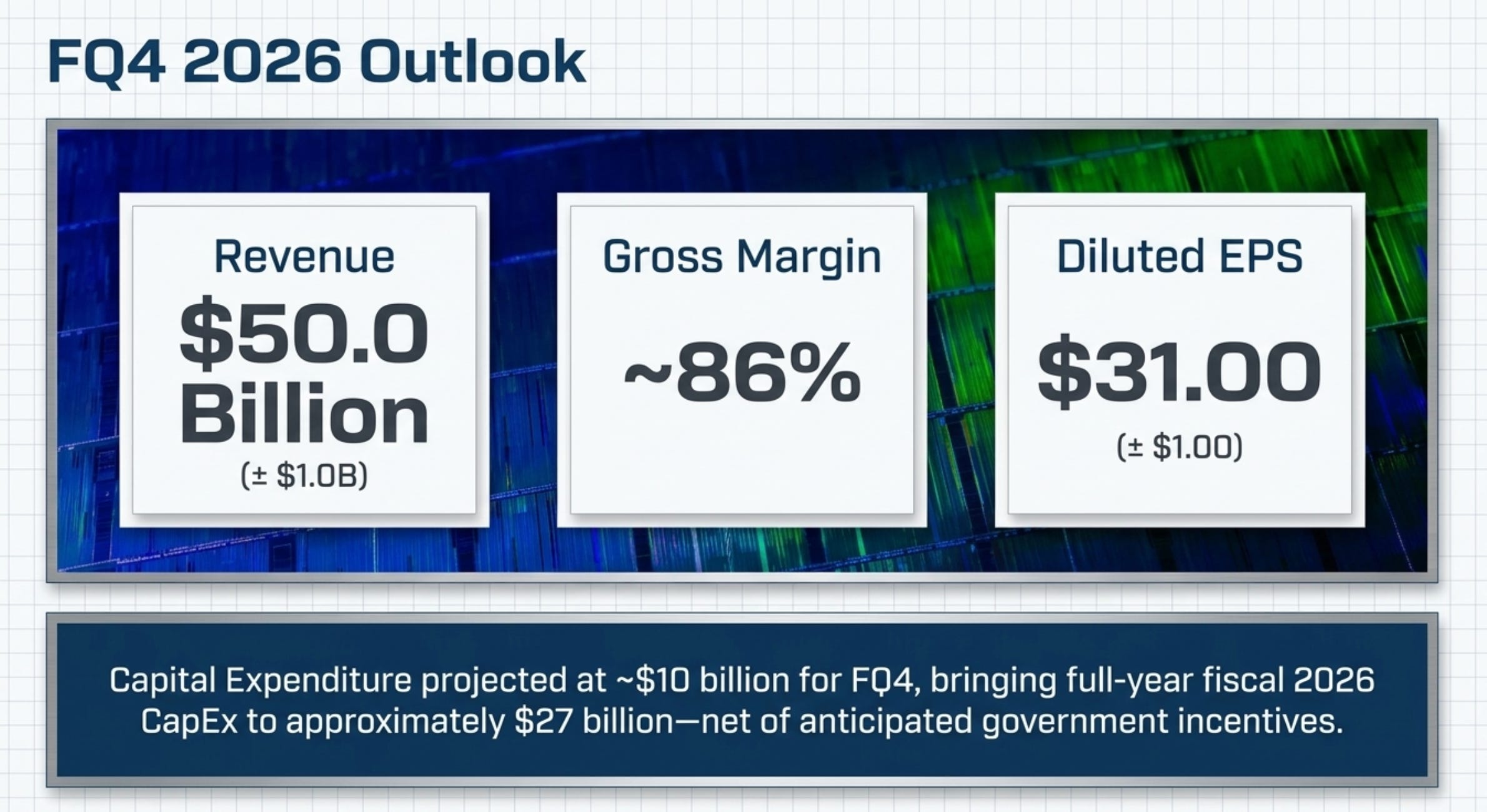

FQ4 2026 Guidance: Revenue at $50.0 billion (±$1.0B) , Gross Margin at ~86% , and Non-GAAP EPS at $31.00. While management noted that the rate of sequential price increases is beginning to moderate, overall profitability continues to expand via high-margin product shifts.

Segment Performance breakdown:

Cloud Memory (CMBU): Hit a record $13.77 billion (+78% Q/Q) with an 83% gross margin.

Core Data Center (CDBU): Reached $11.52 billion (+103% Q/Q) with an 87% gross margin, heavily driven by data center SSD revenue doubling to over $5 billion.

Mobile and Client (MCBU): Generated $11.52 billion (+49% Q/Q) at an 87% gross margin. Price gains completely offset a slight sequential drop in unit bit shipments.

Automotive and Embedded (AEBU): Brought in $4.63 billion (+71% Q/Q) at a 79%

gross margin.

The Invisible Tailwinds

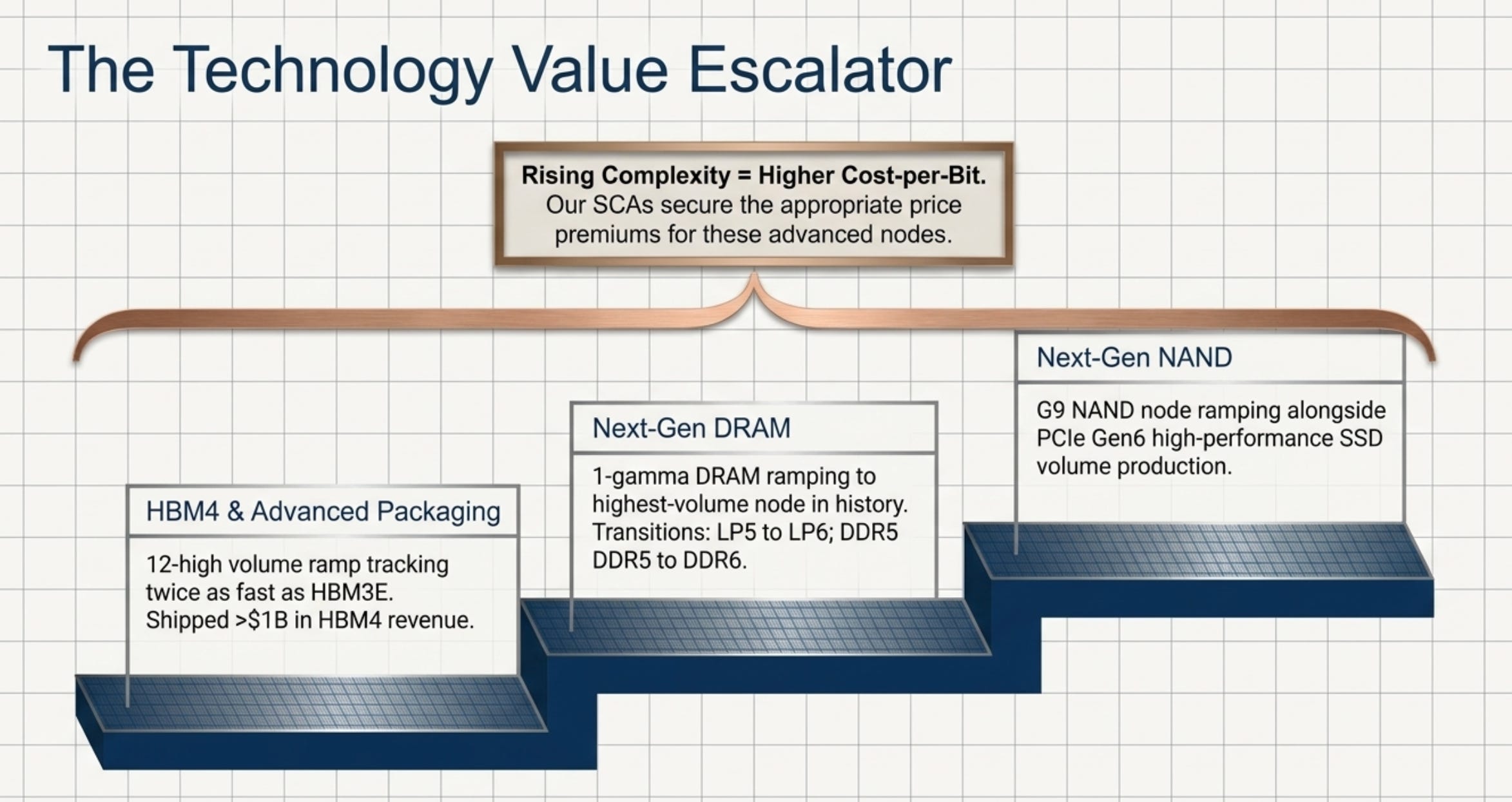

The HBM4 S-Curve: 12-high HBM4 (built on the 1-beta node) volume ramping is pacing twice as fast as the previous HBM3E generation. Micron has already cleared over $1 billion in pure HBM4 revenue. Commercial, high-volume yields are tracking to hit maturity significantly faster than HBM3E.

The Multi-Decade Humanoid Trigger: Wall Street’s financial models currently value Micron strictly as a proxy for hyper-scaler AI data center buildouts. They are completely ignoring the physical AI scaling inflection point coming in late 2027/2028.

The Humanoid Math: While an AI-enabled smartphone utilizes 12GB–16GB of DRAM to run edge models , and an autonomous L2+ vehicle requires roughly a 5x memory multiplier , a single humanoid robot commands a minimum of 10x the memory content of an L2+ vehicle (translating to a massive baseline of 128GB to 256GB of advanced DRAM per unit).

Physical AI cannot rely on cloud computation latency. A commercial humanoid must process terabytes of raw spatial data locally, instantly converting multi-camera computer vision, sensory pressure metrics, and real-time physical simulation into locomotion variables. A humanoid robot is quite literally a walking server rack. When mass manufacturing escalates, global wafer capacity will hit an absolute supply wall, and Micron sits at the center of this structural deficit.

Valuation

Micron’s forward guidance of $31.00 per share in Non-GAAP EPS for FQ4 annualized places the asset’s current baseline earning power at ~$124.00. At a current equity price floating between $1050 and $1090, the stock is trading at an implied forward P/E multiple of just 8.5x to 8.8x. For an infrastructure monopoly with >80% operating margins during an structural supply allocation crunch, this represents a massive mispricing.

At the current price Micron shares are trading at an unjustified discount to the company's new, de-risked business model. Thanks to the contractual elimination of market cycles through the $100 billion Take-or-Pay framework and a forward P/E sitting below 9x, this represents a rock-solid value opportunity at the very core of the AI revolution. Our calculated 12-month intrinsic value for the business stands at $1480–$1550 per share. Any technical pullbacks driven by large institutional profit-taking should be treated as buying opportunities.

Maintain long position.

This publication is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Readers are solely responsible for their own investment decisions. The author is long Micron

cool images, how’d you make them. won’t steal or nothing… 🤍