This Stock Could Rally 50% on the Nuclear Revolution

They’re burning cash, missing earnings—and still might be building the future of energy.

OKLO is a phenomenal stock. With market cap $3.5B it's burning cash and falling in double digits after the disappointing earnings. Oklo reported a net loss of $73 million in 2024, more than double its $32 million loss in 2023. Nevertheless, the stock gained 25% YTD and 140% in a year. Some analysts see it gaining 50% by the next March and the company itself tells investors about the significant investments and calls for patience.

What's the secret? The company has two powerful resources. Nuclear power and nuclear lobby. Most companies of its size can only dream of the people who can regularly meet president Trump in person. He's the first official you'll see in Oklo presentation, below current Energy Secretaary Chris Wright.

Chris Wright was the Oklo Board member, and the other guy with enormous power is the founder Sam Altman, Boss of the OpenAi. He owns near 2.6% of startup that makes his share worth $60M.

A big spender

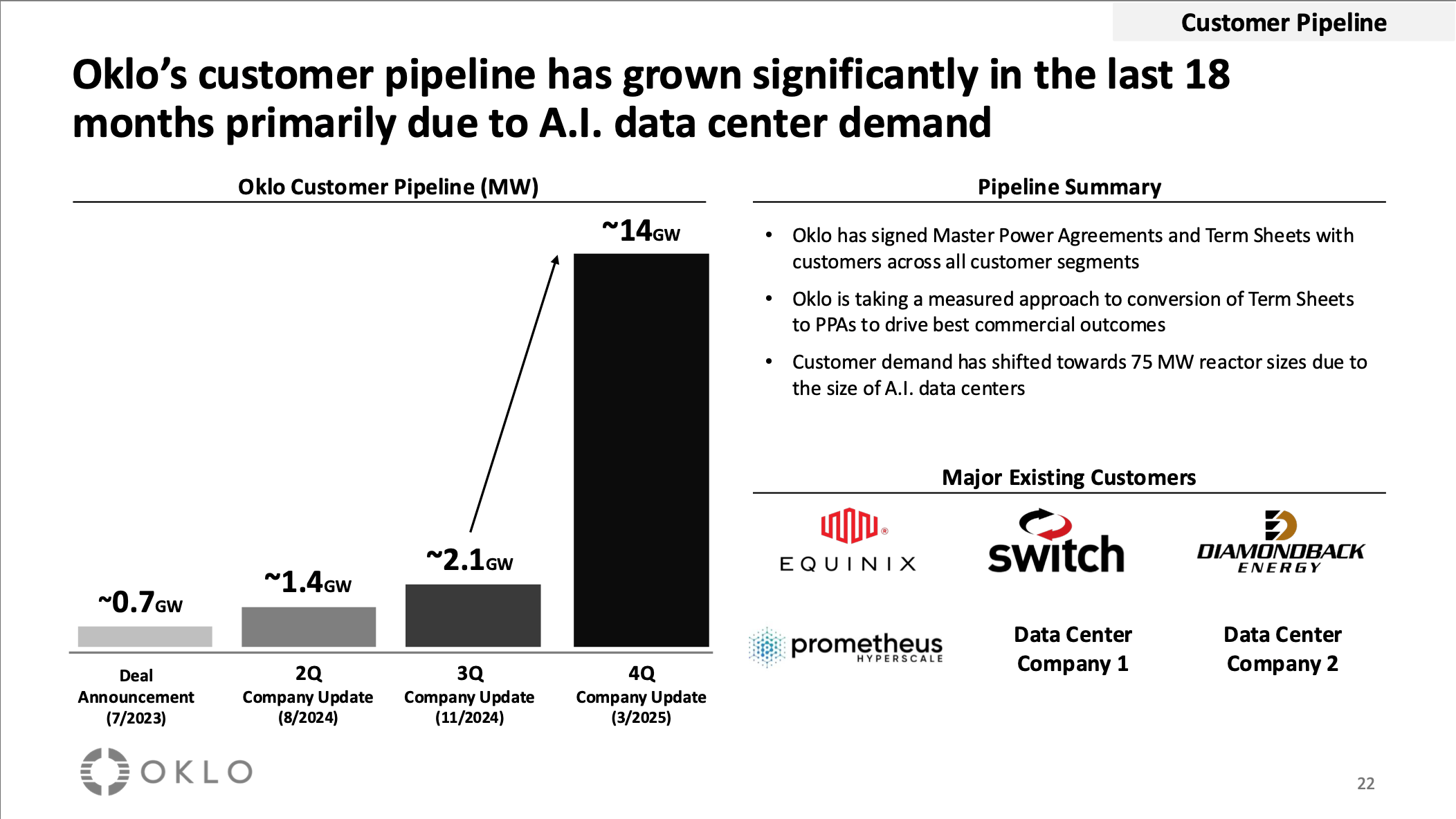

Oklo released worse than expected earnings, widening losses to $73M in 2024 from $32M in 2023. The stocks plummeted 16% in two days with the weak market, trading at $26, two times less than at its peak. The main message to investors - we will spend and spend, don't wait too much until 2027. The company has secured a 12-gigawatt master agreement with Switch, as well as interest from Equinix and Diamondback Energy. These are not binding power purchase agreements, but they do indicate early alignment with major infrastructure players.

"We’ve already made big strides in 2025: evolving our powerhouse offering to scale up to 75 MW, partnering with RPower on a gas-to-nuclear strategy, and expanding into radioisotope production with our strategic acquisition of Atomic Alchemy. These moves unlock new revenue opportunities and open additional market for Oklo", said Jacob DeWitte, Founder & CEO.

Atomic Alchemy, recently acquired by Oklo, specializes in the production of radioisotopes used for medical, research, and industrial applications. While it's a niche field, it complements Oklo’s existing nuclear capabilities and expands its addressable market beyond power generation. The deal positions Oklo to enter the radioisotope supply chain, a critical and often under-resourced segment of the nuclear sector. If successful, this could provide an additional revenue stream in the near term—something Oklo badly needs to offset its capital-intensive build-out phase. The radioisotope market is estimated to be in excess of $55B by 2026.

Oklo is developing compact, modular nuclear reactors aimed at serving high-demand energy users, particularly AI and cloud data centers. The reactors are designed for a "build, own, operate" model, where Oklo will maintain ownership and sell power under long-term agreements. Importantly, Oklo has made a strategic decision to scale its reactors to the 60–75 megawatt range. This decision was driven by demand from large energy users. According to the company, this power level aligns well with data center infrastructure, particularly at the data hall level, and reduces the number of reactors needed for gigawatt-scale deployments.

Cutting the red tape

The company has also received a construction permit for its project at Idaho National Laboratory, which may provide a regulatory edge as it moves toward commercialization.

Altman, who chairs the board, is closely aligned with the energy demands of the AI sector. As OpenAI moves toward building its own data centers, the integration of nuclear power becomes a strategic consideration. Nuclear energy offers reliability and scalability for compute-heavy infrastructure. Oklo has enormous interest from investors after the sensational growth of nuclear plant owners CEG and Vistra. They struggle with the whole market but this trend is irreversible.

Oklo's proposition fits within a broader trend where AI leaders seek control over their entire stack: from chips to compute to energy. If this vertical integration materializes, Oklo could be positioned as a key supplier.

Oklo has two core advantages: nuclear energy technology and deep political access. Few early-stage companies of its size have individuals on their board with direct access to the upper levels of government.

The White House next door

The former Board member Chris Wright—is the current Energy Secretary. Sam Altman promised Trump to build multibillion Stargate project, I won't be surprised to see synergy, it will need a lot of energy. Even if not so, Altman has vast resources and direct access to Trump. People invest in political connections, it's another "Palantir" case.

A new board member Dan Poneman served as U.S. Deputy Secretary of Energy from 2009 to 2013 and was most recently CEO of Centrus Energy, a major nuclear fuel supplier.

Also on the board is Michael Thompson, founding partner of Reinvent Capital, which previously backed SpaceX. His presence is notable given Elon Musk’s historic tension with Altman and OpenAI. That he’s supporting Altman’s nuclear play suggests that Oklo is not just building reactors—it’s assembling a lobbying and capital war chest.

Nuclear risks

If you invest in any cash-burning company, you take the risk. If we take OKLO, let's take some of them into consideration. We have to understand that its venture and hype is over. The market is volatile and unprofitable stocks are burning first. So far I see the risks:

No revenue-producing product

Unproven commercial technology

Dependence on favorable regulation and fuel availability

However, the demand signal from the AI and data center sectors is real. The energy footprint of next-generation compute infrastructure is growing rapidly. If Oklo can deliver on even part of its promise, it could play a significant role in that ecosystem. The current stock performance reflects both the uncertainty and the long-term optionality. We already made comparisons to energy companies like Vistra and Constellation, which have benefited from the AI narrative and infrastructure tailwinds.

This is not a momentum trade. Oklo is an early-stage company with high capital needs and long development cycles. But its strategic alignment with one of the most important trends in global infrastructure—the intersection of AI and energy—warrants attention.

We cover new tech not because it's safe, but because it's directional. Oklo is risky, but it reflects where markets and policy might converge over the next decade. It's a company to understand now, even if the payoff takes time. The last price targets imply big upside for OKLO with $30 from Citi and as high as $45 from Wedbush and $43 from Craig-Hallum.

This publication is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Readers are solely responsible for their own investment decisions. The author may hold positions in the securities mentioned.