Oracle ($ORCL): The Meta-Morphosis. Why Larry Ellison is Chasing 40% Margins in the AI Cloud Era

The Quest for the $1T Club through Radical Transformation: No Room for Error.

On March 31, Oracle initiated a massive global headcount reduction, axing somewhere between 20,000 and 30,000 employees. According to TD Cowen, these cuts target $8B to $10B in annual savings.

But does this strategy actually move the needle?

To put this into perspective: according to the latest filings, ORCL 0.00%↑ is burdened with $165 billion in total long-term liabilities. Even a $10 billion cost-cutting program fails to address even 10% of that debt mountain.

The company has maintained its characteristic lack of transparency, declining to comment on the restructuring. However, TD Cowen analysts suggest the primary target is the Healthcare division, a unit Oracle acquired for $28 billion that has yet to deliver, as major clients reportedly migrate to competitors like Epic.

With the stock having surrendered nearly half of its peak market capitalization, we need to determine if Oracle is a deep-value play or if the market offers better risk-adjusted alternatives. We won’t bore you with a summary of Oracle’s business model; instead, we are diving straight into the balance sheet of the most leveraged infrastructure play in the sector.

Growth at Any Cost

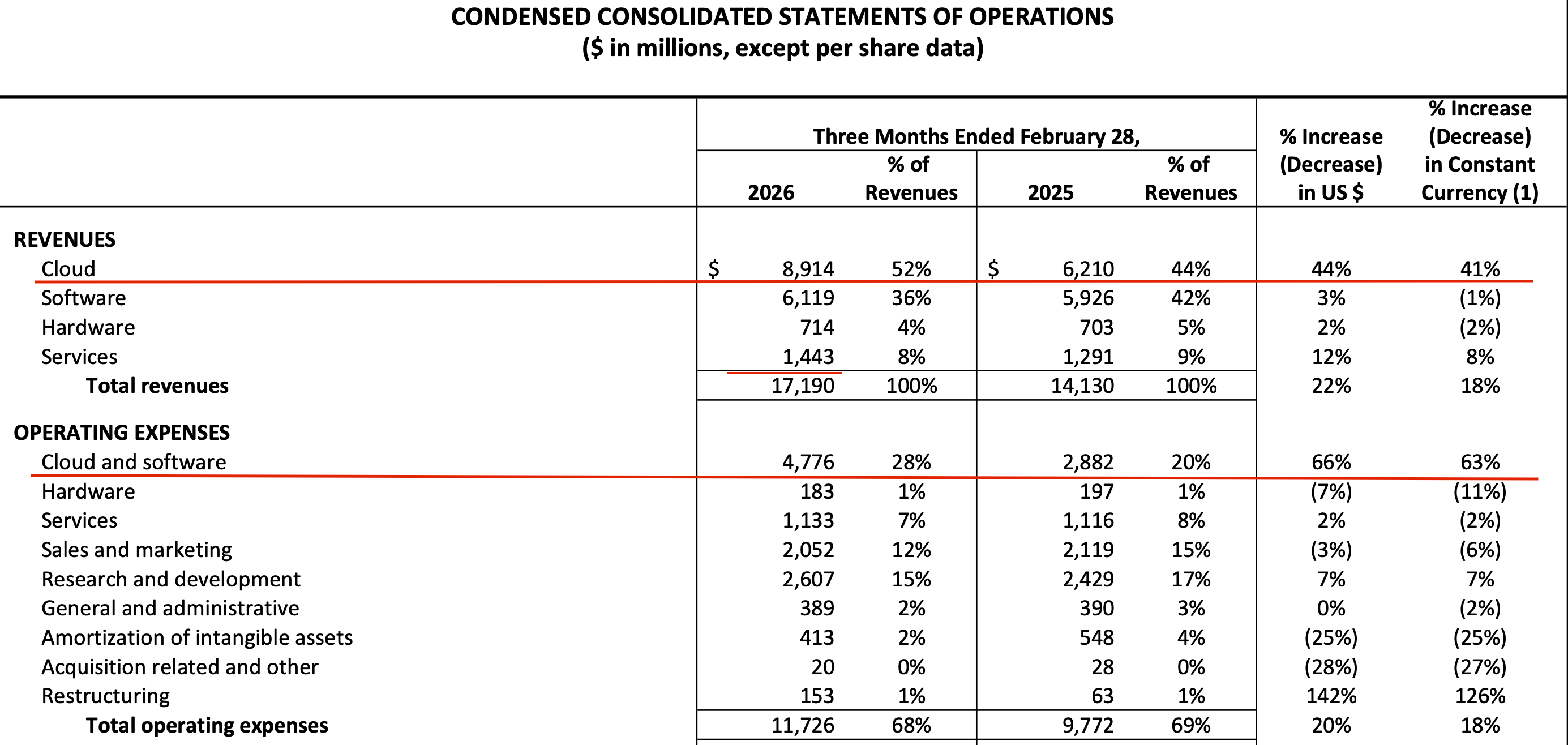

Oracle’s Q3 2026 earnings print presents a masterclass in financial engineering and narrative distraction. On the surface, the numbers look robust: total revenue climbed 22% YoY to $17 billion. Dig deeper, and the cracks in the legacy model become craters. Half of that top line, $8.9 billion, is now categorized as Cloud Revenue, up 44%. However, investors must realize this isn’t organic expansion; it is growth aggressively subsidized by a ballooning debt load.

The engine behind these numbers is the massive build-out of data centers saturated with NVDA 0.00%↑ GPUs. This segment is exploding at an 84% clip, yet it remains the most capital-intensive part of the business. This is precisely why Oracle is burning through cash and leveraging its balance sheet to the hilt. While cloud infrastructure specifically for databases - Exadata and Autonomous Database - posted a respectable 35% gain, it is increasingly overshadowed by the “dumb pipe” hardware business.

This aggressive pivot is reflected in the staggering 66% surge in Cloud and Software operating expenses, which hit $4.7 billion. This is the price of admission for the AI era: Oracle is front-loading massive costs and accepting short-term margin pressure to ensure it doesn’t get left behind. It is a ruthless reallocation of capital, funded by a “clearing of the decks” that includes 30,000 layoffs, all to finance the infrastructure required to stay relevant.

On the software side, Cloud Applications (SaaS) are growing in the mid-teens. While this outpaces peers like CRM 0.00%↑, it is fundamentally insufficient to sustain a premium multiple in an AI-driven market. Oracle’s reporting remains intentionally convoluted, designed to highlight growth silos while masking the decay of the core.

The sobering reality is that Oracle’s entire software portfolio - including databases, legacy applications, and support - eked out a meager 3% increase. In constant currency, that’s effectively stagnant. Wall Street, currently gripped by a “SaaS Apocalypse,” is dumping Oracle alongside the likes of NOW 0.00%↑ and CRM. This is a massive failure of Investor Relations. The company has failed to articulate the reality that it is no longer a software firm, it is undergoing a desperate, high-stakes structural pivot.

The transformation is as dramatic as it is existential: Oracle is being forced to abandon its software roots to survive an era where Anthropic and other AI pioneers are making traditional enterprise code obsolete. They aren’t just changing; they are fleeing a dying industry.

David vs. Goliath: A Fight Oracle Can’t Outspend

The shift in Oracle’s financial engineering is nothing short of drastic. For the past decade, the company was an ATM for its shareholders, deploying $123 billion toward share buybacks. Today, that trend has inverted. To fuel its massive AI infrastructure ambitions, Oracle has pivoted to a $20 billion ATM equity offering, a move that directly dilutes shareholders and pressures future EPS.

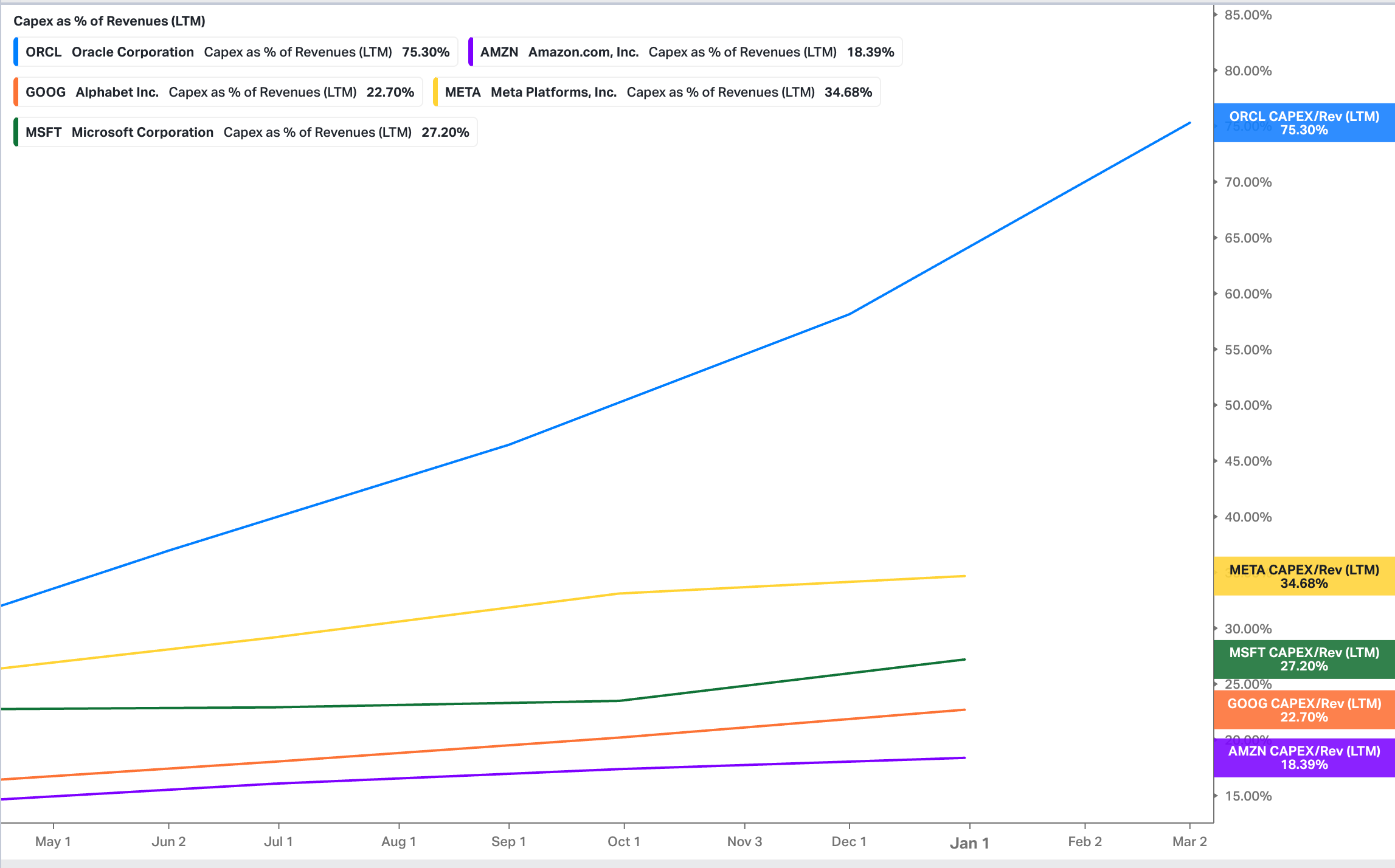

The scale of this ‘all-in’ bet becomes clear when compared to the industry titans. While Google Cloud’s quarterly revenue of $17.66 billion matches the entirety of Oracle’s top line, the financial breathing room between the two is vast. As shown in the data, Google maintains a disciplined 22.7% CapEx-to-revenue ratio, funding its expansion through its massive operational cash engine. In contrast, Oracle is operating at a breakneck 75% ratio.

By spending three-quarters of its total revenue on Capital Expenditures, Oracle has effectively traded its status as a reliable dividend-and-buyback play for a high-stakes seat at the AI table. It is competing with Big Tech resources it simply doesn’t have on the balance sheet, forcing a total overhaul of its fiscal policy to keep pace in a race where the entry fee has never been higher.

For the first time in 30 years, Oracle has plunged into negative Free Cash Flow territory. With a TTM negative FCF of $24.74 billion - equivalent to roughly two full years of the company’s net income - the market’s anxiety is becoming visible. Oracle’s 5-year Credit-Default Swap (CDS) recently spiked to 125 basis points, its highest level in three years, signaling that the cost of insuring Oracle’s debt against default is rising alongside its ambitions.

Keep reading with a 7-day free trial

Subscribe to Edge of Power to keep reading this post and get 7 days of free access to the full post archives.