Google won. How much time will Apple lose?

Apple’s management is suffocating the company. Will it follow the path of the rival it once crushed in court?

Google’s courtroom victory — and a fresh all-time high for its stock — teaches a very simple lesson: if you have enough money, you can do almost anything, even turn history around. Just three months ago, the stock took a sharp hit after Apple VP Eddy Cue told the very same court that search queries in Safari were declining. And yet, here we are.

Gemini may lag behind ChatGPT, but Google is moving AI search forward. You already feel it — no more killing time digging for the right link.

Waymo keeps expanding, its network growing with no real rival. The program is capital-intensive; total spend may already exceed $10B. It still doesn’t show up in the financials, but the process is alive. No Tesla-like hype — because there’s no driver in the seat. Apple shut down its car project after years of failure.

Android evolves alongside Samsung’s foldables — something Tim Cook’s team still can’t crack. And search is very much alive: Google posted $96B in revenue and $28B in profit last quarter, even with AI chatbots, agents and assistants attacking from all sides.

I don’t even fully understand how it works, because I’m used to ChatGPT — but who am I to argue with the market? The main reason is clear: chatbots hallucinate too much, while Google lets you fact-check with AI on top. YouTube and ads keep printing money, and now Google Cloud is gaining weight — $13B last quarter.

And don’t forget TPUs — pretty much the only chips out there that can stand up to NVIDIA. Built quietly, without glossy Forbes spreads like Amazon’s.

So what’s the point of all these examples? Simple: with deep enough resources, you can either bury a company (like BlackBerry, whose downfall was as much about bad lawyers as bad products) — or you can push it to a new level.

AI isn’t just about research — it’s about money. And the law of large numbers favors those who can spend. As an investor, that’s the lesson. I learned it the hard way: I sold almost all my Google stock, then had to buy back after their strong earnings a few months ago — on a smaller scale.

The real takeaway: big companies always have cards up their sleeve. They can play them when no one expects it — when analysts are already writing obituaries. It could be a new product line, an acquisition, a radical shift. Nvidia “invented” AI (at least for Wall Street). MongoDB proved software still matters. Carvana is somehow still selling cars.

All different scales, of course — because nothing compares to Google. But with resources mobilized, a turnaround is always possible. Sometimes investors just need patience — and a little faith in management.

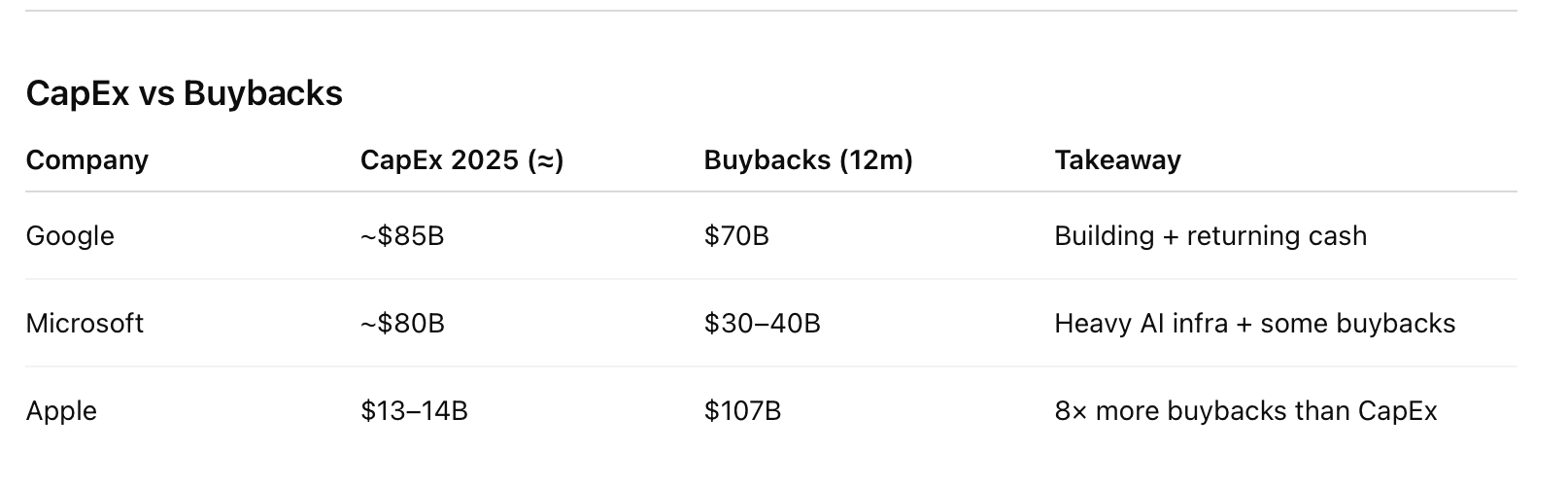

Apple spends 8× more on buybacks than on building the future. Google and Microsoft are mobilizing billions for AI infrastructure. Apple is busy engineering EPS.

The Microsoft Lesson

When Satya Nadella took over in 2014, Microsoft was stagnant. Ten years later:

+969% stock growth.

Azure at ~$147B run-rate.

Deals with OpenAI and Activision Blizzard.

Copilot putting AI inside Office and Windows.

That’s what happens when leadership actually commits capital and strategy.

So why not Apple?

The company has the money, but instead of chasing new frontiers, it sinks billions into buybacks. Apple gets praised for corporate governance, ESG, diversity. But behind it sits a board with no interest in growth. That’s the only explanation for why Tim Cook remains untouchable while the company flatlines.

Google is +20% YTD. Apple is +3%.

Even the people who were running Apple’s ghost AI projects have moved to Meta. When was the last time you heard of anyone joining Apple? It has turned into a closed club, not a leader.

Could Apple still surprise? Sure. They could buy Perplexity. Order 100,000 NVIDIA GPUs. Snap up Firefly. Flip the narrative.

I still hold a big Apple position. But every quarter, the hope for a miracle fades. Court wins don’t come every day.

This publication is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Readers are solely responsible for their own investment decisions. The author may hold positions in the securities mentioned.

It seems Apple is sleepwalking while Google is rewriting the script.

It’s an entrepreneur problem. What to do with the free cashflow? By betting on a takeover like the ones you suggested (for which they would most certainly overpay, everyone knows they have the money), they would forego a certain small improvement in the per share numbers. Do you risk crashing your stock price on a bet which, if it turns out well sets the company up for the next 10 years or do you keep tinkering on the edges, making small improvements in what will eventually become a dead end street?