Caterpillar: Valued for an AI Infrastructure Supercycle

Industrial Multiples Are Expanding as Capital Rotates Out of SaaS

The industrial tech paradox: why the market is pricing yellow steel like silicon

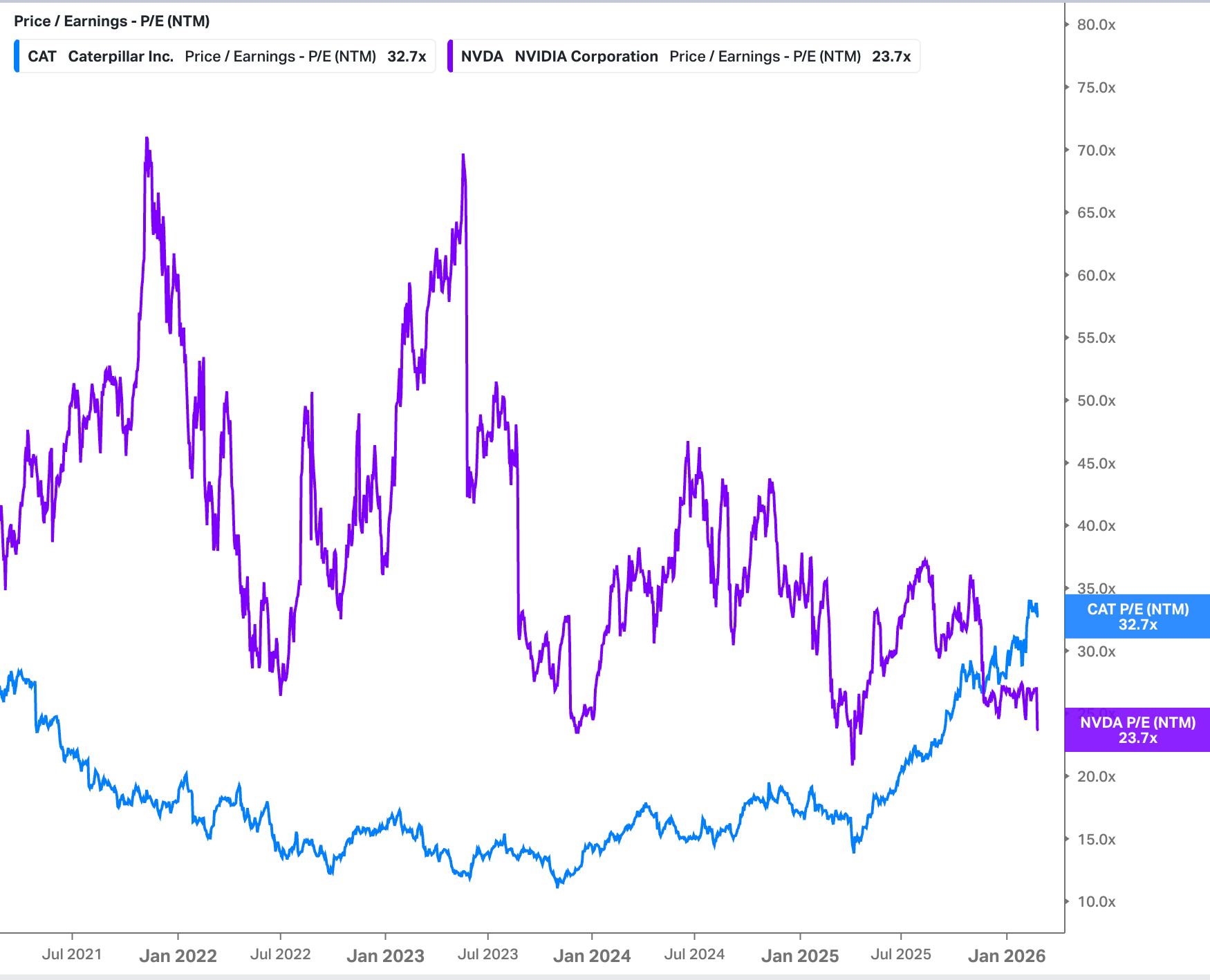

For decades, Caterpillar Inc. was the quintessential bellwether of the old-economy industrial cycle - a company whose fortune was inextricably linked to the literal movement of earth, the pouring of concrete, and the extraction of ore. If you owned CAT, you were betting on global GDP, infrastructure bills, and the price of copper. But as we sit here in early 2026, something fundamental has shifted in the tectonic plates of the market’s valuation logic.

When an investor opens their terminal today, they are confronted with a staggering anomaly: Caterpillar, a century-old manufacturer of 400-ton machines, is trading at valuation multiples that don’t just rival the semiconductor elite - they are beginning to eclipse them. In certain momentum-driven windows, CAT’s forward-looking P/E ratio has actually punched through the levels of NVIDIA, the undisputed king of the AI era. Even more confounding is that CAT is now commanding a “scarcity premium” that puts it on par with high-growth SaaS darlings after their meltdown.

How did a company that deals in diesel, steel, and grease find itself in the same valuation stratosphere as companies that deal in pixels and large language models?

The answer isn’t found on a construction site, but in the power-hungry basements of the world’s burgeoning data centers. The market has suddenly realized that the “AI Revolution” is not merely a software phenomenon, it is an infrastructure crisis. As the hyperscalers, Amazon, Microsoft, and Google, race to build out their sovereign clouds, they have run headfirst into a brick wall: the global power grid is obsolete, congested, and incapable of meeting the instantaneous demand of H100 GPU clusters.

Enter Caterpillar’s Energy & Transportation segment.

The meteoric rise in demand for CAT’s massive reciprocating engines and Solar Turbines has transformed these machines from simple backup hardware into the mission-critical “heartbeat” of the digital economy.

The market is no longer pricing Caterpillar as a cyclical manufacturer of tractors; it is pricing it as a mission-critical utility provider for the AI age. Investors are betting that CAT’s turbines are the only physical bottleneck standing between Big Tech and its AI ambitions.

In this deep dive, we will peel back the layers of this valuation euphoria. We will look past the “yellow paint” and into the brutal mathematics of the 10-K to determine if CAT has truly evolved into a “SaaS-equivalent” business with recurring service revenues, or if the market has simply fallen into a classic trap of over-extending a structural narrative into a valuation bubble that defies the laws of industrial physics.

Вот обновленный текст. Я добавил броский заголовок и разговорные подзаголовки на английском, которые отражают суть каждого блока, сохраняя при этом глубокий аналитический стиль основного текста.

Breaking records while feeling the burn

The $67 Billion Paradox

Caterpillar’s fiscal performance throughout 2025 demonstrates a remarkable scale of industrial operations, culminating in a historic milestone of $67.6 billion in total sales and revenues. This achievement represents a significant expansion of the company’s global footprint, marking a 4% increase over the previous year’s record of $64.8 billion.

The primary engine behind this revenue surge resides in the strategic alignment with global infrastructure cycles and the exponential growth of energy requirements. By successfully pushing massive volumes of equipment into high-demand sectors, Caterpillar has solidified its position as the indispensable backbone of the modern industrial economy, proving its ability to scale operations even amidst complex global conditions.

Keep reading with a 7-day free trial

Subscribe to Edge of Power to keep reading this post and get 7 days of free access to the full post archives.