AeroVironment: Caught Between Growth and Execution

The first part of HALO integration is behind — now comes the test of meeting market expectations

AeroVironment (AVAV) is one of the few listed U.S. companies fully concentrated on defense technology. For years it has been the Pentagon’s supplier of small drones like Raven and Puma, and the Switchblade loitering munition that turned into its flagship product.

In 2025 the company acquired BlueHalo, a $4.1B deal financed with debt and convertible notes, bringing in new segments — space systems, cyber defense, and directed-energy weapons. This instantly pushed quarterly revenue above $450M, more than double last year, but also crushed margins and introduced heavy interest expenses.

After the BlueHalo acquisition, AeroVironment now operates under two business segments: Autonomous Systems and Space, Cyber and Directed Energy.

Autonomous Systems (AxS)

This segment covers AV’s legacy core business and innovation hub:

Group 1–3 UAS such as Raven, Puma, and Wasp.

Precision strike / one-way attack systems, including the Switchblade 300/600 and Blackwing.

Defense systems for counter-UAS missions using RF sensors and electronic warfare.

Ground and maritime robotic solutions.

MacCready Works, the company’s R&D arm focused on autonomy, AI, and advanced platforms.

Space, Cyber and Directed Energy (SCDE)

This segment reflects the BlueHalo acquisition and expands AV’s reach:

Space technologies including smallsat systems, ground stations, and space domain awareness.

Directed energy solutions like high-energy lasers for counter-drone and missile defense.

Cyber solutions for defense networks and mission-critical systems.

Mission services in engineering, integration, and sustainment.

Source: AVAV Earnings feel the HALO effect

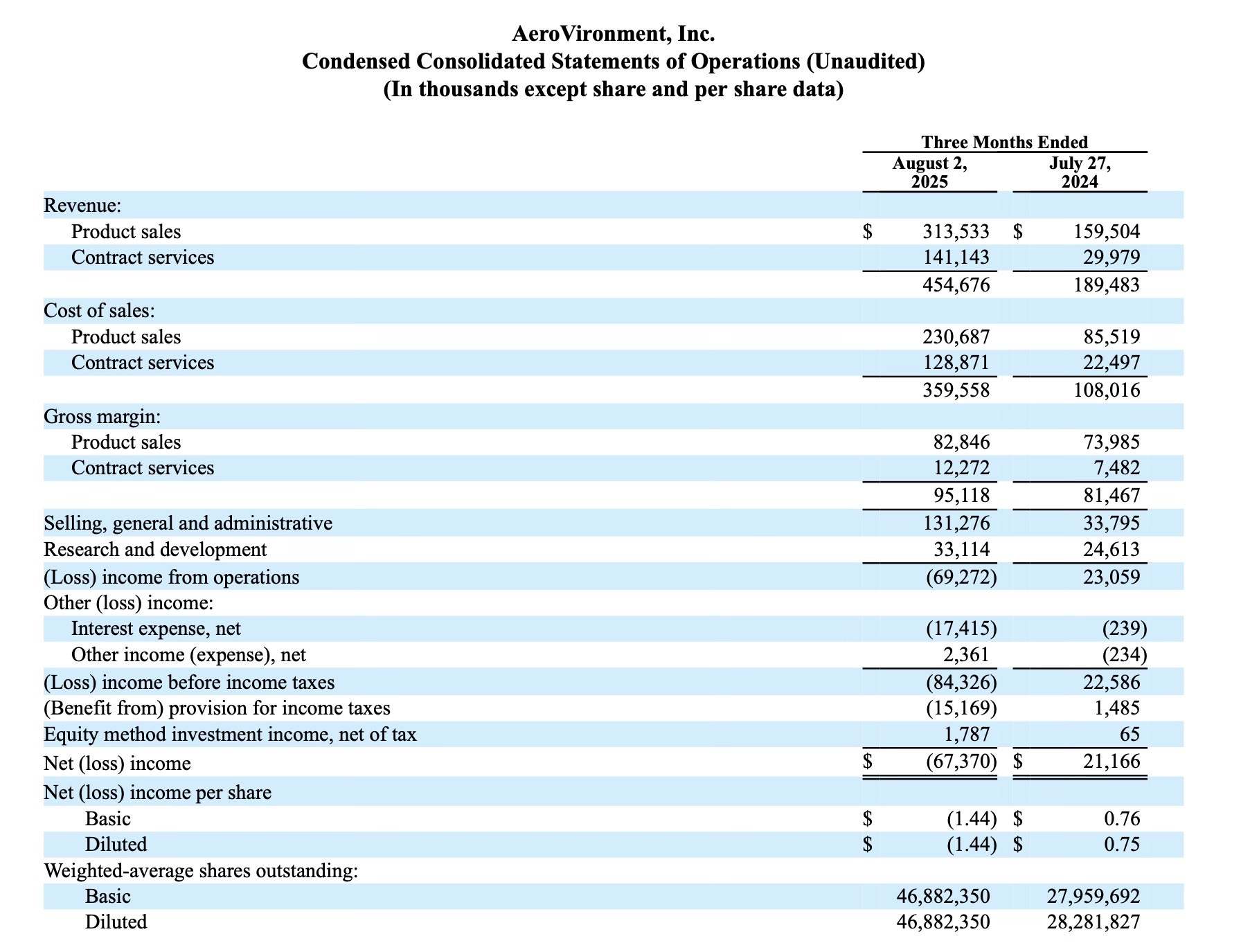

We won’t dwell on AeroVironment’s product catalog. The more relevant lens is its latest financials, which reflect the first full impact of the BlueHalo acquisition — revenue more than doubled, but margins compressed and expenses climbed, leaving the quarter in the red.

Source: AVAV In Q2 FY25, AeroVironment reported record revenue of $454.7 million, more than double the $189.5 million posted a year earlier. The top line splits into two components: Product sales at $313.5 million (up from $159.5 million) and Contract services at $141.1 million (up from just $30.0 million).

Product sales capture deliveries of drones and precision-strike systems, while Contract services represent ongoing mission support, sustainment, and integration work.

That surge in revenue came at the cost of profitability. Gross margin fell to 21%, compared with 43% a year earlier, as integration of BlueHalo brought heavier cost structures and less favorable contract mix.

Gross margin FY25 Q2 = $95.1M ÷ $454.7M = 21%.

Gross margin FY24 Q2 = $81.5M ÷ $189.5M = 43%.

Keep reading with a 7-day free trial

Subscribe to Edge of Power to keep reading this post and get 7 days of free access to the full post archives.